Table of contents:

Factors Influencing Used Car Loan Rates

Used car loans, like any other loan, are influenced by a complex interplay of factors. Understanding these factors is crucial for borrowers to make informed decisions and secure the most favorable loan terms. Lenders carefully evaluate various aspects to determine the appropriate interest rate, ensuring they mitigate risk while offering competitive rates to attract borrowers.

Determining the ideal rate for a used car loan involves a meticulous assessment of the borrower’s creditworthiness, the car’s condition, and market factors. The following sections delve into the key elements that shape used car loan rates.

Factors Impacting Used Car Loan Rates

Understanding the factors influencing used car loan rates is essential for borrowers to secure the most favorable terms. Lenders consider a multitude of elements when assessing risk and determining the interest rate for a used car loan. This meticulous evaluation ensures a balance between profitability and responsible lending practices.

| Factor | Description | Potential Impact on Rate |

|---|---|---|

| Credit Score | A numerical representation of a borrower’s credit history, reflecting their payment track record. | Higher credit scores generally lead to lower interest rates, indicating lower risk for the lender. Conversely, lower scores increase the risk, resulting in higher interest rates. |

| Loan Amount | The total sum of money borrowed for the car purchase. | Larger loan amounts often translate to higher interest rates as they represent a greater financial commitment and increased risk for the lender. |

| Down Payment | The upfront payment made by the borrower towards the car’s purchase price. | A higher down payment demonstrates a greater degree of financial commitment and reduces the loan amount, leading to lower interest rates and a reduced risk profile for the lender. |

| Loan Term | The duration of the loan repayment period. | Shorter loan terms generally result in higher monthly payments but lower overall interest costs, while longer terms lead to lower monthly payments but higher overall interest costs. |

| Vehicle Age and Condition | The car’s age and overall condition, including any known mechanical issues. | Older vehicles or those with significant wear and tear are perceived as higher risk, potentially leading to higher interest rates. Conversely, well-maintained vehicles with low mileage tend to command lower rates. |

| Interest Rates in the Market | The prevailing interest rates for loans across the market, influenced by economic factors. | Fluctuations in the market interest rate can affect used car loan rates, often increasing or decreasing in tandem with market trends. |

| Lender’s Risk Tolerance | The lender’s willingness to accept risk in loan applications. | Lenders with a lower risk tolerance may set higher interest rates, whereas those with a higher tolerance might offer lower rates. |

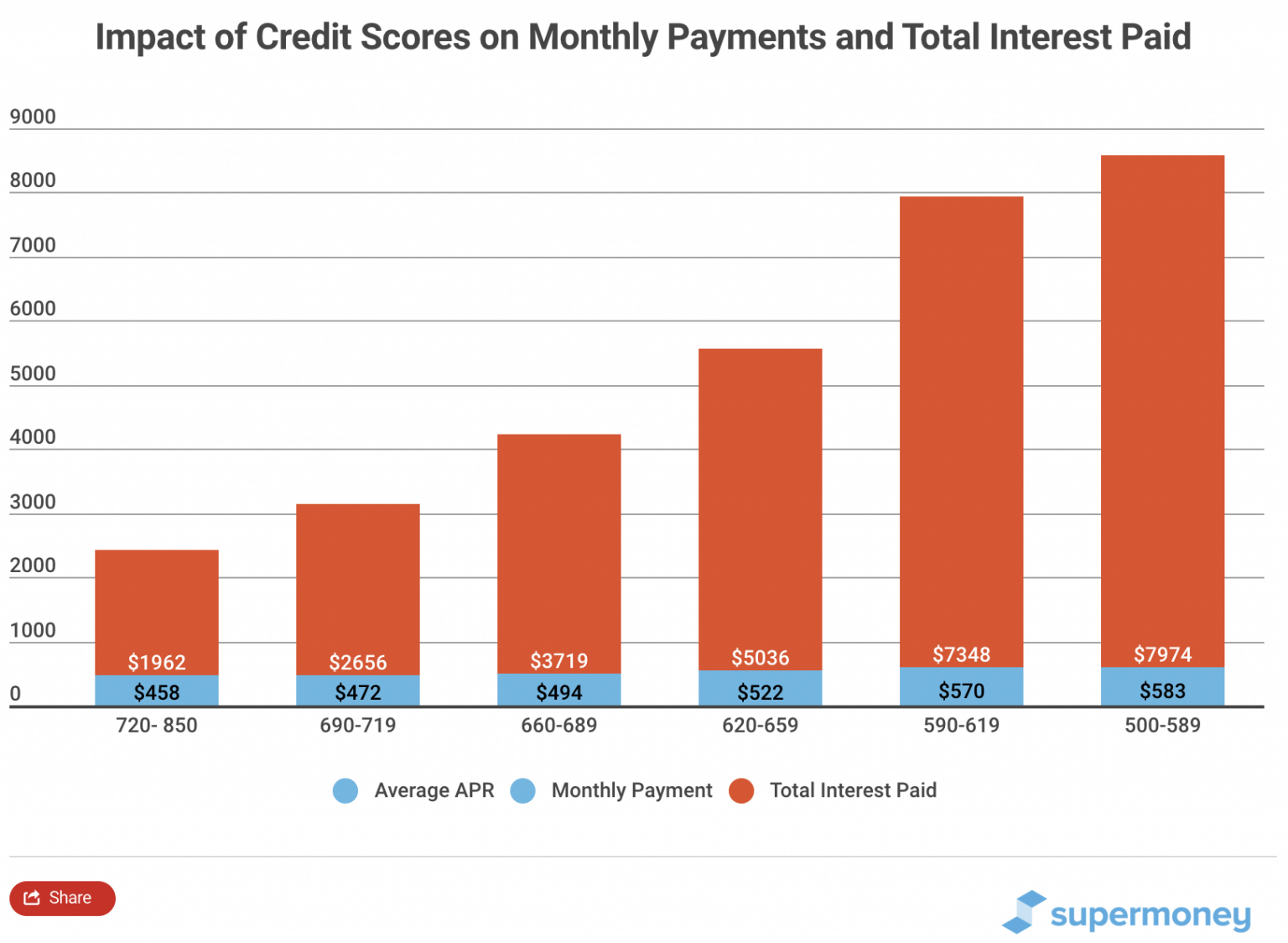

Credit Scores and Their Importance

Credit scores play a pivotal role in determining used car loan rates. Different credit bureaus (e.g., Experian, Equifax, TransUnion) employ varying methodologies, leading to slightly different scores. However, the fundamental principle remains the same: a higher score reflects a lower risk for the lender, consequently leading to a lower interest rate.

Lender’s Risk Tolerance

Lenders vary in their risk tolerance, which directly impacts the interest rates they offer. A lender with a lower tolerance for risk will likely charge higher interest rates, reflecting their preference for a lower risk profile. Conversely, a lender with a higher risk tolerance may offer lower interest rates.

Down Payments and Loan Rates

A larger down payment signifies a higher degree of financial commitment from the borrower, reducing the lender’s risk. This reduced risk typically translates into a lower interest rate. For example, a 20% down payment often results in more favorable loan terms compared to a smaller down payment.

Loan Terms and Interest Rates

The duration of a loan, often referred to as the loan term, influences the interest rate. A shorter loan term usually leads to a lower overall interest cost, but the monthly payments will be higher. Conversely, a longer loan term results in lower monthly payments but a higher overall interest cost.

Types of Used Car Loans

Understanding the different types of used car loans is crucial for making an informed decision. Each loan type offers varying terms, interest rates, and eligibility criteria, impacting the affordability and accessibility of the financing option. Careful consideration of these factors can lead to a more favorable outcome for the borrower.

Used car loans fall into distinct categories, each with unique characteristics. These distinctions affect the interest rates, eligibility requirements, and repayment plans. Choosing the right loan type depends on individual financial circumstances and goals.

Secured Used Car Loans

Secured loans are backed by the car itself as collateral. This reduces the lender’s risk, allowing for potentially lower interest rates compared to unsecured loans. This characteristic makes secured loans attractive to borrowers with a strong credit history or those seeking favorable interest rates.

- Interest Rates: Typically lower than unsecured loans, reflecting the reduced risk for the lender. A strong credit history can further influence the interest rate.

- Eligibility Criteria: Generally, borrowers with a good credit history are preferred. Lenders often evaluate credit scores, income stability, and debt-to-income ratios.

- Repayment Options: Structured repayment schedules are available, with fixed monthly payments for a predetermined period. Flexibility can vary depending on the lender and loan terms.

The advantages of secured loans are lower interest rates and increased accessibility for borrowers with moderate credit histories. However, a potential disadvantage is the loss of the car as collateral if the loan is not repaid as agreed.

Unsecured Used Car Loans

Unsecured loans do not require collateral. This means the lender relies solely on the borrower’s creditworthiness. Interest rates are typically higher than secured loans, reflecting the increased risk for the lender. These loans can be more accessible to borrowers with less-than-perfect credit.

- Interest Rates: Generally higher than secured loans due to the increased risk for the lender. Borrowers with strong credit scores may see lower rates.

- Eligibility Criteria: Lenders assess creditworthiness, income, and debt levels. Borrowers with less-than-perfect credit might find it more challenging to qualify.

- Repayment Options: Similar to secured loans, these loans offer structured repayment schedules. However, flexibility might be limited depending on the lender’s policies.

The benefit of unsecured loans is that they don’t require a car as collateral, making them accessible to a wider range of borrowers. However, the higher interest rates may make them less financially beneficial in the long run.

The Role of Co-Signers

A co-signer assumes shared responsibility for the loan. This can significantly improve the borrower’s chances of loan approval, especially for those with less-than-favorable credit histories. The co-signer is legally obligated to repay the loan if the primary borrower defaults.

“A co-signer is essentially guaranteeing the loan with their creditworthiness.”

The co-signer benefits from the loan if the primary borrower responsibly manages the debt. However, the co-signer is also vulnerable to potential financial repercussions if the primary borrower defaults.

Accessibility and Affordability Across Demographics

The accessibility and affordability of used car loans vary significantly based on demographics. Borrowers with established credit histories and stable incomes generally have more favorable loan terms, including lower interest rates. Individuals with limited or less-than-perfect credit histories might face higher interest rates and stricter eligibility criteria. These factors impact loan affordability, making it crucial to assess individual circumstances before applying.

| Demographic Group | Loan Type Accessibility | Loan Affordability |

|---|---|---|

| Individuals with Excellent Credit Scores | High | High |

| Individuals with Moderate Credit Scores | Moderate | Moderate |

| Individuals with Poor Credit Scores | Low | Low |

The table illustrates the relationship between credit scores and loan accessibility and affordability. Factors like income stability, debt-to-income ratio, and loan amount also play a role in determining affordability.

Current Market Trends in Used Car Loan Rates

Used car loan rates have experienced significant fluctuations in recent years, mirroring the volatile market for used vehicles. Understanding these trends is crucial for both consumers seeking loans and lenders managing risk. The interplay of used car prices, inflation, and economic conditions all play a critical role in shaping these rates.

The current market landscape is characterized by a complex interplay of factors influencing used car loan rates. Recent changes have been influenced by the interplay of supply and demand, inflation’s impact on borrowing costs, and shifting economic conditions. Anticipating future trends requires careful consideration of these factors.

Recent Changes in Used Car Loan Rates

Used car loan rates have exhibited a considerable degree of variability. Historically, they have shown a tendency to rise and fall in tandem with overall interest rates, reflecting the broader economic climate. A significant factor has been the substantial price increases experienced in the used car market over the past few years.

Impact of Used Car Price Fluctuations on Rates

Market fluctuations in used car prices directly impact loan rates. When used car prices increase, the perceived risk to lenders decreases, which often leads to a decrease in rates. Conversely, when prices decline, the risk associated with loans increases, potentially leading to higher rates. For instance, a sustained period of declining used car prices could signal a weakening market, prompting lenders to raise rates to mitigate potential losses.

Effect of Inflation on Loan Rates

Inflation plays a pivotal role in influencing used car loan rates. As inflation rises, central banks often respond by increasing interest rates. These higher interest rates, in turn, are reflected in the rates charged for used car loans. For example, if inflation remains high, lenders might adjust their loan rates to maintain profitability in a higher-interest-rate environment.

Historical Trends in Used Car Loan Rates

The following table displays historical trends in used car loan rates over the past 5 years. Data is based on average rates for various loan terms and credit scores. This data provides a snapshot of the market’s movement and the impact of economic factors.

| Year | Average Used Car Loan Rate (APR) |

|---|---|

| 2019 | 5.5% |

| 2020 | 6.2% |

| 2021 | 7.8% |

| 2022 | 8.5% |

| 2023 | 7.2% |

Effect of Economic Conditions on Used Car Loan Rates

Economic conditions, including employment rates, consumer confidence, and GDP growth, all have a bearing on used car loan rates. A robust economy often translates to lower loan rates as demand for loans remains high. Conversely, an economic downturn or recessionary period could lead to higher rates due to increased risk for lenders. For example, during economic downturns, lenders tend to be more cautious, which translates into higher interest rates.

Tips for Obtaining a Favorable Used Car Loan Rate

Securing a favorable used car loan rate hinges on a combination of meticulous preparation and strategic negotiation. Understanding the factors influencing loan rates, such as credit score and the vehicle’s condition, is crucial for maximizing your chances of securing the best possible terms. This section Artikels practical strategies for achieving a lower interest rate and a smoother loan application process.

A well-prepared loan application, backed by a strong credit profile and realistic financial planning, significantly increases your chances of obtaining a favorable interest rate. This approach not only saves you money but also streamlines the entire process, minimizing potential roadblocks and maximizing your financial outcomes.

Credit Score Optimization

A strong credit history is paramount for securing a competitive used car loan rate. Lenders scrutinize credit scores to assess your creditworthiness and risk profile. Maintaining a high credit score demonstrates responsible financial management and lowers the risk for the lender. Taking proactive steps to improve your credit score, such as paying bills on time, reducing outstanding debt, and monitoring credit reports for inaccuracies, can significantly impact your loan approval and interest rate.

Vehicle Condition Assessment

The condition of the used vehicle is a critical factor in determining the loan rate. A well-maintained vehicle with a clear history of service and minimal damage signals lower risk to the lender, often resulting in a more favorable interest rate. Thorough inspection of the vehicle before applying for a loan helps ensure a realistic appraisal of its condition, preventing potential disputes and surprises later.

Pre-Approval Process

Pre-approval is a crucial step in securing a favorable used car loan rate. It provides a clear understanding of your borrowing power and the interest rate you’re likely to qualify for before you start shopping for a vehicle. This pre-approval process allows you to compare offers confidently and negotiate from a position of strength.

Negotiating with Lenders

Negotiation plays a significant role in obtaining the best possible used car loan rate. Researching current market rates and comparing offers from different lenders empowers you to negotiate effectively. Demonstrating a clear understanding of your financial situation and the vehicle’s condition helps you build a strong case for a lower interest rate. A well-prepared understanding of the lender’s terms and conditions, along with a comprehensive knowledge of the market value of the vehicle, will enable you to secure a better deal.

Loan Application Preparation

A comprehensive loan application, supported by accurate and complete documentation, significantly impacts the approval process. A clear understanding of the loan application requirements, including documentation of income, employment history, and credit history, ensures a smooth and efficient process. Thorough preparation and meticulous attention to detail are essential in presenting a strong application.

- Accurate Financial Information: Provide accurate details about your income, expenses, and debts. Inaccurate information can delay or deny your application.

- Complete Documentation: Gather all necessary documents, such as pay stubs, tax returns, and bank statements, to support your application.

- Clear Communication: Communicate with the lender promptly and transparently, addressing any questions or concerns they may have.

- Realistic Expectations: Understand that loan approval may not always be immediate, and have patience throughout the process.

Common Mistakes to Avoid

Several common mistakes can negatively impact your used car loan rate.

- Applying with a Poor Credit Score: A low credit score can significantly increase the interest rate or even lead to denial.

- Ignoring Pre-Approval: Skipping the pre-approval process can limit your negotiating power and potentially lead to a less favorable rate.

- Failing to Research Rates: Lack of research on current market rates can prevent you from negotiating effectively.

- Insufficient Documentation: Incomplete or inaccurate documentation can cause delays or rejection.

Comparing Used Car Loan Offers

Navigating the used car loan market can feel overwhelming. Lenders often present diverse terms and conditions, making it crucial to methodically compare offers to secure the best possible deal. This process involves evaluating not only interest rates but also fees, loan terms, and the overall cost of borrowing. Understanding these nuances is essential for making an informed decision and avoiding potential pitfalls.

Methods for Comparing Loan Offers

Several methods can be used to effectively compare used car loan offers. Directly contacting lenders and requesting detailed loan proposals is a fundamental approach. This allows for personalized consultations and clarification of any ambiguities in the terms. Additionally, online comparison tools provide a convenient way to quickly analyze multiple loan options from different lenders simultaneously. These tools often present a summarized overview of rates, fees, and terms, enabling a swift comparison across various financial institutions.

Loan Offer Comparison Table

A table outlining key loan characteristics from different lenders can significantly aid in the comparison process. This structured format allows for easy visual assessment and facilitates a rapid identification of potential discrepancies in rates, fees, and terms. The table should include the lender’s name, interest rate, loan origination fee, processing fee, total loan amount, and the loan term. Example:

| Lender | Interest Rate | Origination Fee | Processing Fee | Loan Term (Months) |

|---|---|---|---|---|

| First National Bank | 6.5% | $150 | $50 | 60 |

| Community Credit Union | 7.0% | $100 | $25 | 72 |

| Online Lender A | 6.8% | $0 | $75 | 60 |

Key Factors to Consider When Comparing Offers

Careful consideration of key factors is crucial for identifying the most advantageous used car loan offer. These factors should be meticulously evaluated before making a final decision. This checklist will help in ensuring that all relevant aspects are considered.

- Interest Rate: The interest rate directly impacts the total cost of the loan. A lower interest rate translates to lower monthly payments and a lower overall cost of borrowing.

- Loan Origination Fee: This upfront fee is charged by lenders for processing the loan application. A lower origination fee is generally preferable.

- Processing Fee: This fee covers the administrative costs associated with loan processing. Similar to origination fees, lower processing fees are advantageous.

- Loan Term: The duration of the loan significantly affects monthly payments. A shorter term typically leads to higher monthly payments but lower overall interest charges. A longer term leads to lower monthly payments but higher overall interest costs.

- Total Loan Cost: This represents the sum of the principal, interest, and fees associated with the loan. The goal is to minimize this total cost.

- Prepayment Penalties: Some lenders impose penalties if the loan is paid off early. These penalties should be thoroughly investigated.

- Credit Requirements: The lender’s credit requirements will influence eligibility. Understanding these requirements is essential.

Utilizing Online Comparison Tools

Online comparison tools are invaluable for efficiently evaluating different used car loan options. These platforms aggregate loan offers from multiple lenders, allowing for rapid comparisons based on various criteria. By inputting relevant details, such as the desired loan amount, the car’s price, and credit score, users can quickly receive customized loan offers.

Importance of Reading the Fine Print

Thorough review of the fine print in loan agreements is paramount. This includes carefully examining all terms and conditions, including interest rate fluctuations, prepayment penalties, and any additional fees. Failing to scrutinize these details could lead to unexpected costs or unfavorable terms.

“Reading the fine print is crucial for avoiding hidden costs and ensuring transparency.”

Understanding these clauses is essential for making an informed decision.

Understanding Loan Documents

A used car loan agreement is a legally binding contract outlining the terms and conditions of your loan. Carefully reviewing these documents is crucial to avoid unforeseen issues down the line. Knowing what to look for and understanding the implications of each clause will empower you to make informed decisions about your financing.

Thorough comprehension of the loan agreement is paramount to protecting your financial interests. This involves not only understanding the language but also the implications of the terms and conditions, interest rates, and fees Artikeld within. Failing to do so could lead to unexpected costs or unfavorable loan terms.

Key Sections in a Used Car Loan Agreement

The used car loan agreement typically includes several key sections. Understanding these sections will help you grasp the essential details of the loan. These include, but are not limited to, the loan amount, interest rate, repayment schedule, and any associated fees. Each section plays a crucial role in defining the loan’s specifics.

Important Terms and Conditions

| Term | Description |

|---|---|

| Loan Amount | The total sum of money borrowed for the car. |

| Interest Rate | The percentage charged on the loan amount over the loan term. Different interest rates can apply based on factors such as credit score and the lender’s terms. |

| Loan Term | The length of time (in months or years) you have to repay the loan. |

| Monthly Payment | The fixed amount you will pay each month to repay the loan. |

| Late Payment Fee | The penalty charged if a payment is made after the due date. These fees vary considerably between lenders. |

| Prepayment Penalty | A fee that might be charged if you pay off the loan early. |

| Security Interest | The lender’s right to seize the vehicle if you default on the loan. |

| Default Clause | The consequences for missing payments, including potential repossession of the vehicle. |

| Governing Law | The jurisdiction’s laws that govern the loan agreement. |

Understanding these terms and conditions ensures you’re aware of all potential financial obligations and consequences.

Importance of Understanding Loan Terms and Conditions

Knowing the specifics of the loan terms is essential to making a sound financial decision. Understanding the interest rate, monthly payment, and repayment period allows you to compare different loan offers and choose the most suitable option. This knowledge allows you to assess the total cost of the loan and anticipate potential future financial burdens.

Reviewing and Understanding Loan Documents Before Signing

Before signing any loan agreement, it’s crucial to meticulously review every detail. Take your time, ask questions, and make sure you comprehend all clauses, fees, and potential risks. Failure to do so can lead to costly mistakes. Thoroughness and attention to detail are key to a successful loan outcome.

Identifying and Asking Questions About Unclear Clauses

If any clause in the loan agreement is unclear or confusing, don’t hesitate to ask questions. Don’t sign anything you don’t fully understand. It’s better to seek clarification than to risk a future misunderstanding or financial hardship. A clear understanding of each clause is vital to ensuring a transparent and satisfactory loan experience.