Table of contents:

Loan Qualification Factors

Securing a 72-month used car loan hinges on several key factors. Lenders meticulously assess your financial profile to determine your ability to repay the loan. This evaluation considers your credit history, income stability, and existing debt load. Understanding these factors empowers you to make informed decisions and increase your chances of loan approval.

Factors Influencing Loan Approval

Loan approval hinges on several factors that lenders meticulously consider. Credit history, income, and debt-to-income ratio play a critical role in determining your eligibility.

| Factor | Description | Impact on Loan Approval |

|---|---|---|

| Credit History | A comprehensive record of your past borrowing and repayment behavior. This includes payment history on previous loans, credit cards, and any outstanding debts. | A strong credit history, demonstrating consistent on-time payments, significantly boosts your chances of approval and often results in lower interest rates. Conversely, a history of late payments or defaults negatively impacts approval odds. |

| Income | Demonstrates your consistent ability to generate revenue. Lenders assess your regular income sources and their stability. | A stable and sufficient income stream is crucial for demonstrating your repayment capacity. Lenders will likely scrutinize income documentation, such as pay stubs or tax returns. |

| Debt-to-Income Ratio (DTI) | A measure of the proportion of your income dedicated to servicing existing debts. This includes all outstanding loan payments, credit card obligations, and other debts. | A lower DTI ratio typically indicates a greater capacity to manage additional debt, increasing your chances of approval. Lenders often use a DTI ratio of 43% or less as a benchmark for approving loans. A high DTI ratio suggests a greater risk, potentially leading to rejection or higher interest rates. |

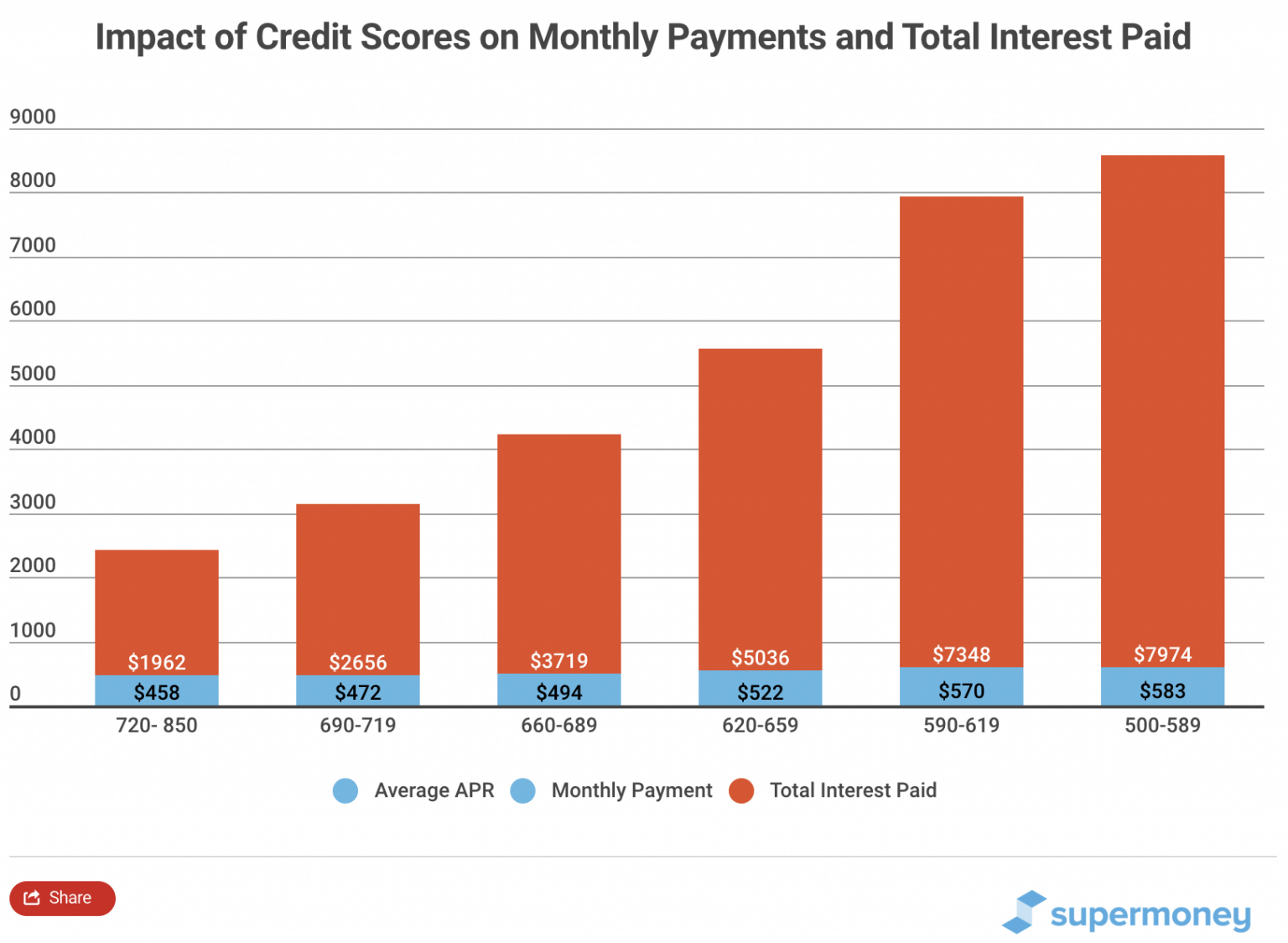

Impact of Credit Score on Interest Rates

Credit scores are a critical factor in determining interest rates for a 72-month used car loan. Lenders use credit scores to assess the risk associated with lending to you.

| Credit Score Range | Interest Rate Range (Example) |

|---|---|

| 660-679 | 7.50%-9.50% |

| 680-699 | 6.50%-8.50% |

| 700-719 | 5.50%-7.50% |

| 720-850 | 4.50%-6.50% |

Note: Interest rates are influenced by several factors beyond credit score, including the prevailing market conditions, the specific lender, and the loan terms. The example rate ranges provided are illustrative and not exhaustive.

Interest Rate Trends

Used car loan interest rates are constantly fluctuating, influenced by a complex interplay of economic factors. Understanding these trends is crucial for both borrowers and lenders to make informed decisions. Recent market conditions have seen rates adjust, impacting the affordability and accessibility of car loans.

Current 72-month used car loan interest rates typically fall within a range of 7% to 12%, varying significantly based on creditworthiness and specific loan terms. This range reflects the current economic climate and the overall demand for used cars. Comparing this range to rates from the past year reveals a noticeable pattern of fluctuation, with rates sometimes increasing and sometimes decreasing.

Typical Interest Rate Range for 72-Month Loans

Interest rates for a 72-month used car loan demonstrate a significant variability, influenced by factors such as credit history, loan amount, and the current economic conditions. A borrower with excellent credit might secure a loan at the lower end of the spectrum, while a borrower with a less-than-perfect credit history might face higher interest rates. The precise rate is usually determined by a lender’s underwriting process.

Comparison with Other Loan Terms

The loan term directly correlates with the interest rate. Shorter terms, such as 60 months, often come with lower interest rates compared to longer terms like 72 months or 84 months. This difference is due to the risk associated with lending over a longer period. Lenders typically charge a higher interest rate for a longer loan term to compensate for the increased risk of potential default over the extended period. For example, a 60-month loan might have a rate of 6.5% to 11%, whereas a 72-month loan could be 7% to 12%, and an 84-month loan might be 7.5% to 13%.

Factors Impacting Recent Changes in Rates

Several factors contribute to the fluctuation of used car loan interest rates. Economic conditions play a pivotal role, as periods of economic uncertainty or recession often result in higher interest rates. Inflation also significantly impacts rates, as rising prices generally lead to higher borrowing costs. The supply and demand of used cars in the market can also affect rates. A low supply of used cars relative to demand can push rates upward. For instance, a sudden surge in demand for a particular model or brand of used car could lead to increased interest rates for that particular model or brand.

Loan Options and Fees

Navigating the used car loan landscape can feel overwhelming. Understanding the different financing options and associated fees is crucial for making an informed decision. This section explores the various avenues for securing a loan, from dealer financing to private party loans, and details the common fees you might encounter. By comparing terms and costs, you can effectively choose the loan that best suits your needs and budget.

Different financing avenues offer distinct advantages and disadvantages. The choice of loan type often depends on factors such as your credit history, the vehicle’s price, and the dealer’s policies. Thorough research and careful consideration of the potential costs are essential.

Dealer Financing Options

Dealer financing, often offered through in-house lending institutions, is a common choice for used car purchases. This method usually provides streamlined processing and potentially lower interest rates for buyers with good credit. However, dealerships often have specific criteria for eligibility and may not always offer the most competitive rates.

Private Party Loans

Securing a loan from a private lender, such as a bank or credit union, allows for more negotiation and potentially better interest rates compared to dealer financing, especially for buyers with strong credit profiles. However, this process usually involves more paperwork and a more extended approval timeframe. It’s essential to carefully review the terms and conditions before committing to a private party loan.

Common Loan Fees

Several fees are typically associated with used car loans. These costs can significantly impact the overall loan cost and should be considered carefully.

- Origination Fees: These fees cover the administrative costs associated with processing the loan application. They are typically a fixed percentage or a flat amount, and can range from a few hundred dollars to several thousand depending on the loan amount and terms. For example, a $20,000 loan might incur an origination fee of $300.

- Prepayment Penalties: Some loans include penalties for paying off the loan before the agreed-upon term. These penalties can vary significantly, from a few hundred dollars to several thousand dollars, depending on the loan agreement. Consider the potential impact of a prepayment penalty when evaluating different loan options.

- Late Payment Fees: Late payments can incur substantial fees, often calculated as a percentage of the missed payment amount. These fees can quickly add up, so maintaining consistent payments is crucial to avoid unnecessary costs.

Loan Option Comparison

This table Artikels the key differences between dealer financing and private party loans, focusing on interest rates, fees, and terms. This information can assist you in making an informed decision based on your individual circumstances.

| Loan Type | Interest Rates | Fees | Terms |

|---|---|---|---|

| Dealer Financing | Typically slightly lower for good credit, but potentially higher for those with lower credit scores. | Origination fees, documentation fees, potential prepayment penalties, and late payment fees. | Loan terms are generally set by the dealership and may be less flexible compared to private party loans. |

| Private Party Loan | Potentially lower than dealer financing, especially for strong credit. | Origination fees, appraisal fees (if required), and late payment fees. | Loan terms are usually more flexible, allowing for negotiation of terms and interest rates. |

Shopping Strategies

Securing the best used car 72-month loan rates requires a proactive approach. Understanding the market, preparing your financial profile, and effectively communicating your needs to lenders are crucial steps in this process. This section Artikels effective strategies to navigate the loan application process successfully.

Finding the Best Loan Rates

Comparing quotes from different lenders is essential to securing the most favorable interest rate. Thorough research and comparison are key to finding the optimal loan terms. Lenders often offer different rates based on creditworthiness, loan amounts, and other factors.

- Online Comparison Tools: Utilize online platforms that aggregate loan offers from multiple lenders. These tools allow for quick comparisons of interest rates, fees, and other loan terms.

- Direct Lender Contact: Reach out directly to lenders offering 72-month used car loans. This approach allows for in-depth discussions and potentially personalized loan terms. Direct contact often leads to a better understanding of the lender’s specific criteria and terms.

- Credit Score Check: Obtain your credit score. Understanding your credit score is crucial. A higher credit score typically translates to a lower interest rate. It’s a good practice to check your credit report and score before applying for a loan to identify and correct any errors.

Preparing a Comprehensive Financial Profile

A comprehensive financial profile strengthens your application and demonstrates your ability to repay the loan. This profile should be presented in a clear and organized manner to lenders.

- Income Documentation: Provide verifiable proof of income, such as pay stubs, tax returns, or W-2 forms. Lenders require this documentation to assess your repayment capacity. Consistency and clarity in presenting income documents are important.

- Debt-to-Income Ratio (DTI): Understand your DTI ratio. A lower DTI generally indicates a better ability to repay the loan. Knowing your DTI ratio and demonstrating a healthy ratio will improve your loan prospects.

- Assets and Liabilities: List assets (savings, investments) and liabilities (existing debts). This comprehensive view of your financial situation allows lenders to assess your overall financial standing.

Presenting Your Financial Profile

Presenting your financial profile effectively is crucial. A well-organized and transparent presentation builds trust and confidence in your ability to repay the loan.

- Clear and Concise Documentation: Organize all supporting documents in a clear and easily understandable manner. This will streamline the review process for the lender.

- Professional Presentation: Present your profile with professionalism and attention to detail. This includes using clear and concise language and ensuring accuracy in the provided information.

- Open Communication: Be prepared to answer questions from the lender about your financial profile. Open communication fosters trust and clarity.

Questions to Ask Potential Lenders

Asking the right questions ensures you understand the terms and conditions of the 72-month used car loan.

- Interest Rates and Fees: Inquire about the specific interest rate and any associated fees. Compare different loan offers to ensure you’re getting the best possible rate.

- Loan Terms and Conditions: Understand the terms of the loan agreement, including the repayment schedule, late payment penalties, and prepayment options. Clearly understanding the terms is vital.

- Pre-Approval Process: Inquire about the pre-approval process. A pre-approval can help you narrow down your options and negotiate better terms.

Impact of Down Payments

A significant factor influencing your used car loan is the amount of the down payment. A larger down payment can lead to more favorable loan terms, reducing your overall borrowing costs and monthly payments. Understanding how down payments affect your loan is crucial for making informed financial decisions.

Effect on Interest Rates

Down payments directly influence the interest rate offered by lenders. Lenders assess the risk associated with the loan based on the borrower’s ability to repay. A larger down payment reduces the lender’s risk, as it represents a greater portion of the car’s value that the borrower has already invested. This, in turn, often translates to a lower interest rate, leading to lower overall borrowing costs. The lower interest rate, in turn, results in lower monthly payments.

Effect on Monthly Payments

A higher down payment reduces the principal amount of the loan. This directly impacts the monthly payment, as the amount borrowed is lower. The formula for calculating monthly payments incorporates the principal amount, interest rate, and loan term. A smaller loan amount, resulting from a larger down payment, leads to a smaller monthly payment. This is demonstrably evident in amortization schedules.

Impact on Total Loan Costs

The total cost of the loan is the sum of all interest payments over the entire loan term. A larger down payment reduces the principal amount and, consequently, the interest accrued over the loan’s life. This is a key advantage of a larger down payment. The reduction in the total cost is directly correlated to the reduction in the loan amount.

Comparison of Loan Terms and Costs with Varying Down Payments

The following table illustrates the impact of different down payment amounts on loan terms and costs. This example assumes a $20,000 used car, a 72-month loan term, and a variable interest rate based on creditworthiness.

| Down Payment | Loan Amount | Estimated Interest Rate | Monthly Payment | Total Interest Paid | Total Loan Cost |

|---|---|---|---|---|---|

| $2,000 | $18,000 | 6.5% | $320.50 | $4,000 | $22,000 |

| $4,000 | $16,000 | 6.0% | $280.00 | $3,360 | $19,360 |

| $6,000 | $14,000 | 5.5% | $240.00 | $2,640 | $16,640 |

Note that these are estimated values and actual figures may vary based on individual credit profiles and lender policies. This table demonstrates the significant reduction in total loan costs and monthly payments with larger down payments.

Amortization Schedule Example (Down Payment $4,000)

This amortization schedule demonstrates the principal and interest breakdown over the 72-month loan term with a $4,000 down payment. This schedule illustrates how the portion of each payment going towards principal increases over time.

| Month | Payment | Principal | Interest | Remaining Balance |

|---|---|---|---|---|

| 1 | $280.00 | $220.00 | $60.00 | $15,780.00 |

| 2 | $280.00 | $221.20 | $58.80 | $15,558.80 |

| … | … | … | … | … |

| 72 | $280.00 | $280.00 | $0.00 | $0.00 |

Alternatives to Traditional Loans

Beyond traditional 72-month used car loans, several alternative financing options exist, each with its own set of advantages and disadvantages. Understanding these alternatives can help you make an informed decision, potentially leading to lower monthly payments or more favorable terms. Careful consideration of these options is crucial for securing the best possible financing for your used car purchase.

Exploring alternative financing options provides a broader perspective on your financial choices, enabling you to compare various terms and conditions. Factors like your credit score, income, and desired loan duration influence the most suitable option.

Leasing

Leasing offers an alternative to purchasing, where you pay for the use of the vehicle over a specific period. This often involves lower monthly payments compared to a loan, but you don’t gain ownership of the car at the end of the lease term.

- Pros: Lower monthly payments, potential tax deductions, flexibility in vehicle upgrades, and less responsibility for vehicle maintenance (depending on the lease agreement).

- Cons: You don’t own the car at the end of the lease, mileage restrictions may apply, potential penalties for exceeding the mileage allowance, and the cost of purchasing the vehicle at the end of the lease might be higher than expected.

Other Financing Options

Various financing options outside of traditional loans exist, including dealer financing, online lenders, and credit unions. These alternatives can offer different interest rates and terms, impacting your monthly payments and total cost of the vehicle.

- Dealer Financing: Often offers competitive rates, especially for those with a strong relationship with the dealership. However, rates can vary based on your creditworthiness and the specific deal you negotiate.

- Online Lenders: Can provide competitive rates and quick approvals for some borrowers. They may have stricter eligibility requirements compared to traditional lenders. Transparency regarding fees and terms is important.

- Credit Unions: May offer lower interest rates and more favorable terms for members. However, membership may be required.

Comparing Costs

A crucial aspect of evaluating alternatives is comparing the total cost over the loan term. Monthly payments and total interest paid are key factors.

| Financing Option | Example Monthly Payment (72 months) | Example Total Interest Paid |

|---|---|---|

| Traditional 72-month Loan | $500 | $1,500 |

| Lease | $300 | N/A (since ownership isn’t transferred) |

| Online Lender | $450 | $1,200 |

Note: These are illustrative examples and actual figures will vary based on the specific vehicle, loan amount, interest rate, and other factors.

Impact of Down Payments

Down payments significantly impact the loan amount and, consequently, the monthly payments and total interest paid for all financing options. A larger down payment reduces the loan amount, leading to lower monthly payments and potentially lower total interest costs.

Maintaining a Healthy Credit Score

A strong credit score is crucial for securing favorable loan terms, including used car financing. A higher credit score often translates to lower interest rates, potentially saving you hundreds or even thousands of dollars over the life of the loan. Understanding how to maintain and improve your credit score is a vital step in achieving your automotive financing goals.

A healthy credit score demonstrates responsible financial management to lenders. This reliability influences the interest rate offered, making it a significant factor in your loan approval process. By understanding and implementing strategies for maintaining a good credit score, you can significantly improve your chances of obtaining the best possible used car loan.

Credit Reporting Agencies and Your Score

Credit reporting agencies, such as Equifax, Experian, and TransUnion, compile credit reports that form the basis of your credit score. These reports track your payment history, credit utilization, length of credit history, new credit, and types of credit. A good understanding of how these agencies assess creditworthiness is crucial to maintaining a positive credit score. Each agency uses a slightly different scoring model, but the fundamental factors remain consistent.

Improving Your Credit Score: A Step-by-Step Guide

Maintaining a positive credit score is an ongoing process. Implementing these steps will help you strengthen your creditworthiness over time:

- Monitor Your Credit Report Regularly: Regularly reviewing your credit reports from all three major bureaus helps you identify any errors or inaccuracies that might be impacting your score. Checking your report annually is a proactive step in ensuring accuracy and catching potential issues early.

- Pay Bills on Time: Consistent on-time payments are a cornerstone of a good credit score. Set up automatic payments or reminders to ensure you never miss a due date, even for small accounts. Late payments significantly damage your credit score.

- Manage Credit Card Debt: Keep your credit card utilization low. Ideally, aim to use no more than 30% of your available credit. High credit utilization can negatively impact your score. Prioritize paying down high-interest debt to minimize the impact on your credit score.

- Avoid Unnecessary Credit Inquiries: Applying for numerous credit cards or loans in a short period can signal financial instability to lenders. Limit your credit applications to only when necessary.

- Build a Long Credit History: Start building your credit history early by obtaining a secured credit card or a small installment loan, like a student loan, and consistently making timely payments. The longer your history of responsible credit use, the stronger your score will become.

Strategies for Managing Credit Card Debt

Effectively managing credit card debt is essential for maintaining a healthy credit score. Prioritize paying down high-interest debt, and consider strategies like the debt snowball or debt avalanche methods to accelerate your repayment.

- Debt Snowball Method: This method focuses on paying off the smallest debts first, building momentum and motivation. The psychological satisfaction of eliminating debts provides positive reinforcement for continued repayment.

- Debt Avalanche Method: This approach prioritizes paying off the debts with the highest interest rates first, saving you money in the long run by minimizing interest charges.

The Impact of a Good Credit Score on Loan Terms

A higher credit score often translates to lower interest rates. This can significantly reduce the total cost of your used car loan. Lenders view a good credit score as a sign of responsible financial management and reduced risk, leading to more favorable loan terms. For example, a borrower with a credit score of 750 might secure a loan with an interest rate of 5%, while a borrower with a credit score of 650 might have to accept an interest rate of 7%. The difference in interest rates can translate to significant savings over the life of the loan.