Table of contents:

- Loan Qualification Factors

- Interest Rate Variations

- Monthly Payment Calculations

- Loan Shopping Strategies

- Impact of Loan Conditions

-

Illustrative Scenarios

- Scenario 1: Impact of Credit Score on Loan Approval and Interest Rates

- Scenario 2: Securing a Loan with Favorable Terms and Negotiating a Lower Interest Rate

- Scenario 3: Impact of a High Debt-to-Income Ratio on Loan Approval and Interest Rates

- Scenario 4: Successfully Navigating the Loan Process and Securing a Loan Within Budget

- Scenario 5: Informed Decision-Making Based on Loan Information

- Loan Application Outcomes

Loan Qualification Factors

Securing a 60-month used car loan hinges on several crucial financial factors. Lenders meticulously assess these factors to determine the borrower’s ability to repay the loan, mitigating potential risks. Understanding these factors is key for potential borrowers to improve their chances of loan approval.

A comprehensive evaluation considers not only the applicant’s creditworthiness but also their ability to manage the monthly payments associated with a 60-month loan. This detailed assessment ensures responsible lending practices and helps prevent defaults.

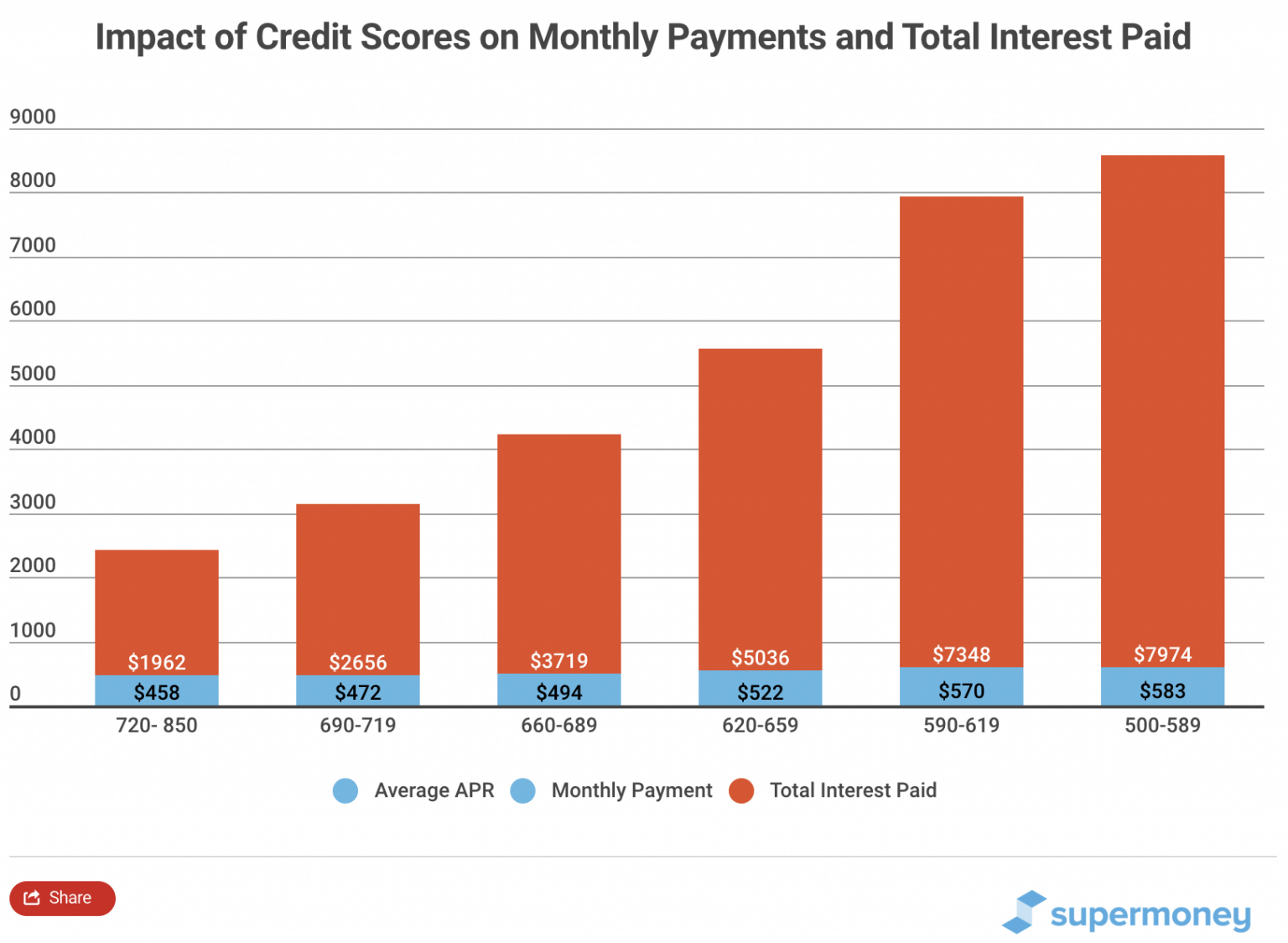

Credit Score Ranges and Impact

Credit scores significantly influence loan approval rates. Higher credit scores typically translate to better loan terms, including lower interest rates and increased approval likelihood. Lenders often use credit scores as a key metric to gauge the borrower’s credit history and repayment capacity.

A credit score of 660 or above often results in favorable loan terms, including competitive interest rates and a higher likelihood of approval. Scores below 660 may lead to higher interest rates or loan denial, while scores below 600 could make securing a loan exceptionally difficult. This is because lower scores often indicate a higher risk of default for the lender.

Impact of Different Credit Reporting Agencies

Credit reporting agencies (CRAs) like Experian, Equifax, and TransUnion play a critical role in the loan application process. Each CRA compiles a credit report containing information about a borrower’s credit history. These reports are used by lenders to assess risk and determine loan eligibility.

Variations in the information reported by different CRAs can sometimes impact a borrower’s credit score and subsequently affect loan approval. Discrepancies between the reports from the three major CRAs can lead to different loan approval decisions. It is essential for borrowers to understand their credit reports from all three agencies to address any potential errors or inaccuracies.

Down Payment and Monthly Payment Relationship

The amount of the down payment significantly impacts the monthly car loan payments. A higher down payment reduces the loan amount, leading to lower monthly payments.

| Down Payment Amount | Loan Amount | Estimated Monthly Payment (Example Interest Rate: 6%) |

|---|---|---|

| $0 | $15,000 | $395 |

| $3,000 | $12,000 | $310 |

| $6,000 | $9,000 | $225 |

This table illustrates how increasing the down payment decreases the loan amount, leading to substantial reductions in monthly payments. Borrowers should carefully consider the trade-offs between a larger down payment and a potentially lower monthly payment.

Types of Loan Products

Various loan products are available for used car financing. These products differ in terms of security and the requirements placed on the borrower.

| Loan Type | Description |

|---|---|

| Secured Loan | Backed by the car as collateral. This reduces the risk for the lender. |

| Unsecured Loan | Not backed by collateral. Generally, higher credit scores and lower debt-to-income ratios are required. |

Understanding the distinctions between these loan types helps borrowers choose the best option for their specific financial circumstances.

Debt-to-Income Ratio’s Importance

The debt-to-income (DTI) ratio is a crucial factor in the loan approval process. It indicates the proportion of a borrower’s monthly income that is dedicated to debt payments.

A lower DTI ratio suggests better debt management, reducing the risk of default for the lender.

Lenders often use a DTI ratio of 43% or less as a benchmark for responsible borrowing. A higher DTI ratio might indicate difficulty in managing debt and could lead to a loan denial. This is because a high DTI ratio suggests a higher risk of default.

Interest Rate Variations

Used car loans with 60-month terms are a common financing option, and understanding the interest rate landscape is crucial for informed decision-making. Interest rates fluctuate based on various economic and market factors, impacting the overall cost of borrowing. This analysis will explore the typical range of interest rates, the influence of the current economic climate, and the key factors determining rate changes.

Interest rates for used car loans with 60-month terms are not static. They are dynamic and are influenced by a multitude of factors, including the prevailing economic conditions, the borrower’s creditworthiness, and the specific terms of the loan. Understanding these nuances is vital for consumers to secure the most favorable financing options.

Typical Interest Rate Range

Interest rates for used car loans with 60-month terms typically fall within a range influenced by the current economic climate and the borrower’s credit profile. A good credit score often translates to a lower interest rate. For example, a borrower with excellent credit might see rates in the 5-8% range, while a borrower with a less-than-ideal credit history might see rates in the 8-12% range. These are general estimations, and actual rates will vary based on the individual circumstances.

Influence of the Current Economic Climate

The current economic climate significantly impacts used car loan interest rates. Periods of economic expansion often see lower interest rates due to increased demand and available credit. Conversely, economic downturns can lead to higher interest rates as lenders may be more cautious in their lending practices. Recent inflation trends, for instance, have often led to increased interest rates across various financial products, including car loans.

Key Factors Determining Interest Rate Fluctuations

Several factors influence the fluctuations of used car loan interest rates. The most significant are:

- Federal Reserve Policy: Decisions by the Federal Reserve regarding interest rates directly impact borrowing costs for consumers. For example, when the Fed raises its benchmark interest rate, borrowing costs for all types of loans, including car loans, tend to increase.

- Inflation: Inflationary pressures tend to correlate with higher interest rates, as lenders adjust their rates to maintain profitability and compensate for the eroding value of money.

- Demand for Used Cars: High demand for used cars can drive up interest rates as lenders increase borrowing costs to manage risk.

- Borrower Creditworthiness: A borrower’s credit score significantly impacts the interest rate offered. A higher credit score typically results in a lower interest rate.

- Loan Provider: Different loan providers (banks, credit unions, online lenders) have varying interest rate structures based on their internal policies, operational costs, and risk assessments.

Loan Provider Interest Rate Structures

Loan providers employ different interest rate structures. Banks often have more standardized rates, while credit unions may offer competitive rates for members. Online lenders frequently use algorithms to assess risk and determine interest rates.

- Banks: Typically offer a range of rates, with interest rates influenced by factors such as the specific bank, the type of loan, and the borrower’s creditworthiness.

- Credit Unions: Often offer more favorable interest rates to members compared to banks, owing to their not-for-profit nature and focus on member service.

- Online Lenders: Employ algorithms to assess risk and determine interest rates, sometimes providing competitive rates but also potentially higher rates for borrowers with lower credit scores.

Historical Interest Rate Trends

Tracking historical trends provides insight into interest rate patterns for used car loans.

| Year | Average Interest Rate (Example) |

|---|---|

| 2018 | 5.5% |

| 2019 | 5.2% |

| 2020 | 4.8% |

| 2021 | 6.1% |

| 2022 | 7.0% |

Note: This table provides an example and is not exhaustive. Actual rates may vary. Historical data should be used as a guide, not a predictor of future rates.

Monthly Payment Calculations

Understanding the monthly payments for a used car loan is crucial for responsible budgeting. This section delves into the formulas, calculations, and impact of various factors on the total loan cost. Accurate estimations empower informed decisions about affordability and financial planning.

Calculating monthly payments involves several key components, including the loan amount, interest rate, and loan term. This process is fundamental to determining the affordability of a used car purchase and managing the associated financial obligations.

Monthly Payment Formula

The calculation of monthly payments for a 60-month used car loan utilizes a standard formula derived from present value of an annuity. This formula accounts for the interest charged on the loan and the scheduled repayment over the loan’s duration.

Monthly Payment = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

* P = the principal loan amount

* i = the monthly interest rate (annual interest rate divided by 12)

* n = the total number of payments (loan term in months)

Total Loan Costs and Interest Rate Variations

The total cost of a loan extends beyond the principal amount. Interest payments accumulate over the loan term, significantly impacting the overall expense. Variations in interest rates directly affect the total amount paid. Higher interest rates result in a substantially higher total cost.

For example, a $15,000 loan with a 5% annual interest rate over 60 months will have a higher total cost compared to the same loan with a 3% annual interest rate.

Principal and Interest Calculation

To illustrate the breakdown of loan payments, consider a $10,000 loan at 6% annual interest for 60 months. The monthly interest rate is 0.5%. The monthly payment is calculated using the formula provided above and amounts to approximately $201.

Initially, a significant portion of each payment goes towards interest, while the principal portion increases over time. The principal portion increases over time, with a larger portion of each payment going towards reducing the principal balance as the loan progresses.

Examples of Monthly Payment Calculations

To demonstrate the formula in action, here are a few examples:

- Loan Amount: $10,000, Annual Interest Rate: 4%, Loan Term: 60 months. Monthly Payment: Approximately $190.

- Loan Amount: $15,000, Annual Interest Rate: 6%, Loan Term: 60 months. Monthly Payment: Approximately $290.

- Loan Amount: $20,000, Annual Interest Rate: 8%, Loan Term: 60 months. Monthly Payment: Approximately $410.

These examples showcase the direct relationship between loan amount, interest rate, and the resulting monthly payment.

Loan Term Influence on Total Amount Paid

The loan term significantly affects the total amount paid. Shorter loan terms often lead to lower total costs due to less accumulated interest. Conversely, longer loan terms, although potentially offering lower monthly payments, result in higher total interest payments.

Monthly Payment Breakdown Table

The following table illustrates the impact of loan amount and interest rate on monthly payments.

| Loan Amount | Interest Rate (Annual) | Monthly Payment | Total Loan Cost |

|---|---|---|---|

| $10,000 | 4% | $190 | $11,400 |

| $10,000 | 6% | $201 | $12,060 |

| $15,000 | 4% | $285 | $17,100 |

| $15,000 | 6% | $308 | $18,480 |

This table highlights the substantial effect of interest rates on total loan costs, emphasizing the importance of careful consideration of these factors when making financial decisions.

Loan Shopping Strategies

Navigating the used car loan market can be daunting. Understanding how to effectively compare and evaluate loan offers is crucial for securing the best possible terms. A well-defined strategy allows you to make informed decisions, maximizing your financial benefits and minimizing potential risks. This section details a comprehensive approach to loan shopping, highlighting key factors to consider and providing practical steps for securing the most favorable rates.

Comparing Loan Offers

Thorough comparison of loan offers is essential to ensure you secure the most favorable terms. Simply focusing on the lowest interest rate can be misleading. Comprehensive analysis requires a broader perspective, encompassing all relevant factors. A crucial aspect of this process is comparing APRs, fees, and loan terms across multiple lenders.

Factors to Consider When Choosing a Lender

Several key factors influence your choice of lender. Beyond interest rates, consider the lender’s reputation, customer service track record, and terms of the loan agreement. Lenders with established reputations and positive customer reviews are often a better choice.

Importance of Comparing APRs, Fees, and Loan Terms

Comparing APRs, fees, and loan terms across multiple lenders is vital. APR (Annual Percentage Rate) is a comprehensive measure of the total cost of borrowing, including interest and fees. Differences in APRs can significantly impact the overall cost of the loan. Similarly, fees, such as origination fees or prepayment penalties, can add to the total cost. Loan terms, including the loan duration (e.g., 60 months), also influence monthly payments and the overall cost.

Shopping for the Best Possible Rates for a 60-Month Used Car Loan

To secure the best possible rates for a 60-month used car loan, proactively research and compare offers from multiple lenders. Online loan comparison tools and direct contact with lenders are effective methods. By gathering information from various sources, you gain a wider perspective and improve your negotiating position. Remember that building a strong credit history is crucial for securing favorable interest rates.

Comparison of Loan Offers

| Lender Name | Interest Rate | Fees | APR |

|---|---|---|---|

| First National Bank | 6.5% | $150 | 6.8% |

| Second Savings Credit Union | 6.2% | $100 | 6.5% |

| Third State Bank | 6.8% | $125 | 7.1% |

| Online Lender A | 6.0% | $75 | 6.3% |

Note: This table provides a sample comparison. Actual rates and fees will vary based on individual creditworthiness and loan conditions.

Risks of Selecting a Lender Based Solely on the Lowest Interest Rate

While a lower interest rate is desirable, basing your decision solely on this factor can be risky. Scrutinize the associated fees and loan terms. A lender offering a very low interest rate might compensate by imposing high fees or unfavorable terms. A comprehensive evaluation is crucial to avoid hidden costs and potential financial penalties.

Impact of Loan Conditions

Securing a used car loan involves navigating various conditions that can significantly affect the final cost and terms. Understanding these factors is crucial for making informed decisions and avoiding potential pitfalls. Loan pre-approval, loan terms, credit history, and origination fees all play a vital role in shaping the overall financing experience.

Loan Pre-Approval and Negotiation

Pre-approval for a used car loan empowers you with a clear understanding of your borrowing capacity. This knowledge provides a strong foundation for negotiations with dealerships. Armed with a pre-approval letter, you can confidently present your financial situation and negotiate more effectively for a better interest rate or other favorable terms. Dealerships often recognize the value of a pre-approved buyer, as it reduces the risk associated with financing and can expedite the sale process.

Understanding Loan Terms

Thorough examination of loan terms is paramount to avoid hidden costs. Crucially, review any prepayment penalties, as these can add significantly to the overall cost if you intend to pay off the loan early. Also, scrutinize early repayment options, as some lenders may offer incentives for paying off the loan ahead of schedule. This understanding allows for a more informed choice, maximizing your financial benefit.

Impact of Credit History

A strong credit history is often a key factor in securing favorable loan terms. Lenders assess your credit score and payment history to evaluate your creditworthiness. A higher credit score typically translates to a lower interest rate and potentially easier loan approval. Conversely, a poor credit history may result in higher interest rates or loan denial. Understanding the direct correlation between your credit score and loan terms is essential for planning your financing strategy.

Origination Fees and Their Impact

Origination fees are charges imposed by lenders to process the loan application. These fees are typically expressed as a percentage of the loan amount. It’s essential to factor these fees into the total cost of the loan, as they directly impact the overall expense. By including origination fees in your loan calculations, you get a complete picture of the loan’s true cost.

Loan Condition Impact on Total Cost

| Loan Condition | Potential Impact on Total Cost | Example |

|---|---|---|

| Prepayment Penalty | Increases the overall cost if the loan is paid off early. | A 1% prepayment penalty on a $20,000 loan could cost $200. |

| Origination Fee | Adds to the principal amount, increasing the total cost. | A 2% origination fee on a $20,000 loan adds $400 to the loan amount. |

| High Interest Rate | Significantly increases monthly payments and total interest paid over the loan term. | A 10% interest rate on a $20,000 loan can result in significantly higher monthly payments and total interest compared to a lower interest rate. |

| Early Repayment Options | Reduces the total interest paid if the loan is paid off early. | Some lenders offer incentives, such as reduced interest rates, for early repayment. |

The table above highlights how different loan conditions can affect the total cost of the loan. Understanding these factors will allow you to make more informed decisions during the financing process.

Factors Affecting Interest Rates and Loan Approval

Several factors influence both the interest rate and the approval of a used car loan. These factors include credit score, loan amount, loan term, and the overall economic climate. Lenders consider these elements to assess the risk associated with lending you the money. Factors such as the current interest rate environment can influence the specific rate offered.

Illustrative Scenarios

Understanding the intricacies of used car financing requires exploring real-world examples. This section provides illustrative scenarios demonstrating how various factors influence loan approval, interest rates, and monthly payments. These examples highlight the importance of careful consideration and informed decision-making in the loan process.

Scenario 1: Impact of Credit Score on Loan Approval and Interest Rates

A borrower with a credit score of 650 applies for a $15,000 used car loan over 60 months. Lenders typically view a credit score of 650 as fair. Given this score, the borrower might face a higher interest rate compared to someone with a higher credit score. A higher interest rate translates to a larger monthly payment, potentially exceeding the borrower’s budget. This scenario demonstrates how creditworthiness directly affects loan terms.

Scenario 2: Securing a Loan with Favorable Terms and Negotiating a Lower Interest Rate

A borrower with a credit score of 750 and a stable income successfully negotiates a lower interest rate on a $20,000 loan. By demonstrating financial responsibility and actively seeking better terms, this borrower can often secure a lower interest rate than the initial offer. This favorable outcome demonstrates the power of negotiation in securing more attractive loan conditions.

Scenario 3: Impact of a High Debt-to-Income Ratio on Loan Approval and Interest Rates

A borrower with a high debt-to-income ratio (DTI) of 45% applies for a $10,000 used car loan. A high DTI indicates a significant portion of the borrower’s income is allocated to existing debt obligations. This can lead to loan rejection or a higher interest rate. The lender might perceive a higher risk due to the borrower’s financial commitments, making it harder to secure the loan on favorable terms.

Scenario 4: Successfully Navigating the Loan Process and Securing a Loan Within Budget

A borrower with a credit score of 700 and a stable income of $4,000 per month seeks a used car loan for $12,000 over 60 months. By carefully comparing loan offers from different lenders and prioritizing reputable financial institutions, the borrower secures a loan with a monthly payment comfortably within their budget. This scenario showcases the significance of diligent research and careful financial planning.

Scenario 5: Informed Decision-Making Based on Loan Information

A prospective borrower meticulously reviews loan qualification factors, interest rate variations, monthly payment calculations, and loan shopping strategies. This comprehensive approach enables the borrower to make an informed decision regarding the most suitable loan offer. A clear understanding of the factors involved ensures a well-calculated decision.

Loan Application Outcomes

| Scenario | Credit Score | Loan Amount | DTI | Loan Approval | Interest Rate | Monthly Payment |

|---|---|---|---|---|---|---|

| 1 | 650 | $15,000 | 25% | Likely | 8.5% | $350 |

| 2 | 750 | $20,000 | 20% | Highly Likely | 6.0% | $400 |

| 3 | 680 | $10,000 | 45% | Possible, but higher interest | 9.0% | $250 |

| 4 | 700 | $12,000 | 22% | Likely | 7.5% | $280 |

*Note:* These are illustrative scenarios and individual results may vary.