Table of contents:

Loan Interest Rate Factors

Used car loan interest rates are influenced by a complex interplay of factors. Understanding these factors is crucial for consumers seeking the most favorable terms. Navigating the landscape of interest rates empowers individuals to make informed decisions and secure the best possible financing options.

Interest rates for 36-month used car loans aren’t static; they fluctuate based on several key determinants. This dynamic nature necessitates a thorough understanding of the factors driving these changes to optimize your borrowing experience.

Impact of Credit Score

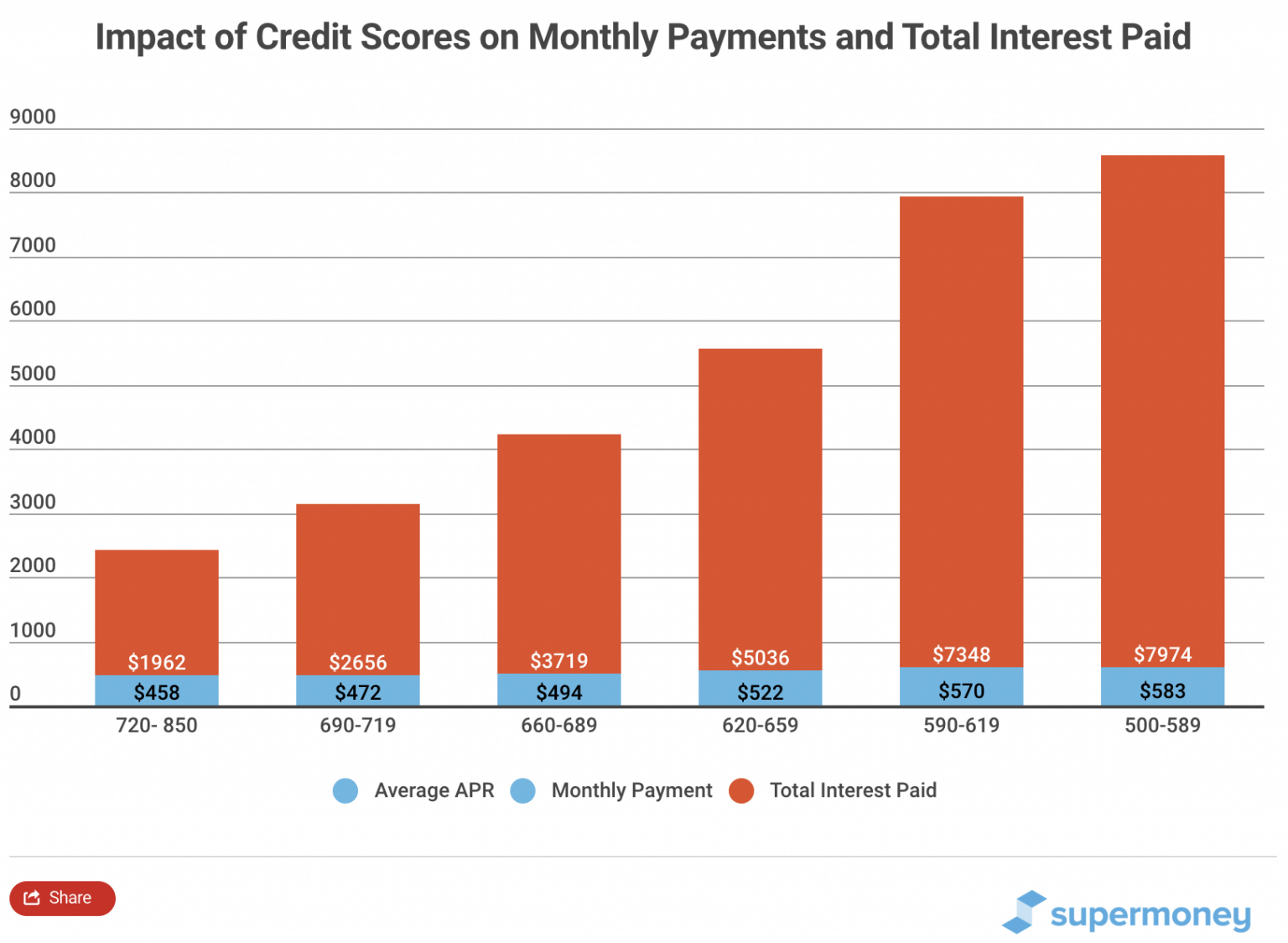

Credit scores significantly impact loan interest rates. Lenders assess creditworthiness to gauge the risk of default. A higher credit score indicates a lower risk, leading to lower interest rates. Conversely, a lower credit score suggests a higher risk, resulting in higher interest rates. This is a fundamental aspect of lending practices, reflecting the established relationship between creditworthiness and risk.

Factors Determining Interest Rates

Several factors contribute to the determination of interest rates. These factors work in concert, creating a complex but predictable system.

- Creditworthiness: Lenders consider credit history, payment history, and outstanding debt when assessing creditworthiness. A strong credit history demonstrates consistent repayment, reducing the risk of default. This is crucial in determining the appropriate interest rate.

- Loan Amount: Larger loan amounts typically come with higher interest rates due to the increased financial risk for the lender. A smaller loan amount represents a lower risk, resulting in potentially lower interest rates.

- Loan Term: Shorter loan terms often result in lower interest rates, as the lender bears the risk for a shorter period. Conversely, longer loan terms increase the lender’s risk, usually resulting in higher interest rates.

- Current Economic Conditions: Economic conditions, such as inflation and interest rate hikes by central banks, can influence the overall cost of borrowing. These external factors have a direct effect on the availability and cost of capital for lenders.

- Market Conditions: Supply and demand in the used car market can impact interest rates. If used car demand is high and supply is low, lenders might charge higher interest rates to reflect the increased risk.

Relationship Between Credit Score and Loan Rates

The relationship between credit score and interest rates is demonstrably strong. A higher credit score generally translates to a lower interest rate. This is because a higher credit score signifies a lower risk of default, making the borrower more attractive to lenders.

Role of Current Economic Climate

The current economic climate plays a crucial role in shaping interest rates. Central bank policies, inflation rates, and overall economic stability influence the cost of borrowing. Periods of high inflation often lead to higher interest rates, as lenders demand higher returns to compensate for the reduced purchasing power of money.

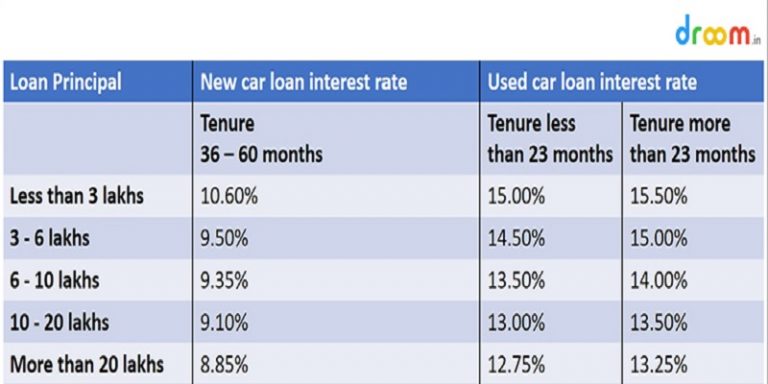

Interest Rate Comparison by Credit Score

| Credit Score | Estimated 36-Month Used Car Loan Rate (Example) |

|---|---|

| Excellent (750+) | 4.5% – 6.0% |

| Good (680-749) | 6.0% – 7.5% |

| Fair (600-679) | 7.5% – 9.0% |

Note: These are illustrative examples and actual rates may vary based on other factors.

Loan Application Process

Securing a used car loan involves a structured application process. Understanding the steps and required documentation is crucial for a smooth and efficient experience. This process typically involves a series of actions, from initial inquiry to final loan approval. Properly completing each step ensures a timely and successful outcome.

Typical Application Steps

The typical application process for a 36-month used car loan follows a sequential series of steps. A streamlined approach reduces delays and enhances the efficiency of the process.

- Initial Inquiry and Pre-Approval: Begin by contacting the lender to inquire about loan options and eligibility. This often involves providing basic information like your credit score, income, and desired loan amount. A pre-approval, if offered, provides a clear understanding of the loan terms and conditions before you shop for a car.

- Car Selection and Negotiation: Once pre-approved, select a used car that aligns with your budget and needs. Negotiate the purchase price with the seller, taking into account the market value and condition of the vehicle.

- Loan Application Submission: Complete the loan application form, providing accurate details about your financial situation and the chosen vehicle. This form will typically request personal information, employment details, and financial history.

- Document Submission: Submit the necessary documents, which may include proof of income, identification, and credit history.

- Credit Check and Loan Evaluation: The lender conducts a credit check to assess your creditworthiness and evaluate the loan application. This evaluation considers your credit history, income, and debt-to-income ratio. Lenders use this information to determine your risk as a borrower and whether the loan terms are appropriate for your financial profile.

- Loan Approval or Denial: Based on the evaluation, the lender approves or denies the loan. If approved, the terms and conditions of the loan are finalized, including the interest rate, loan amount, and repayment schedule. A denial often involves a follow-up discussion to understand the reason and explore possible solutions.

- Funding and Closing: Upon approval, the funds are transferred to the seller, and the necessary paperwork is finalized to complete the loan. The final step is signing all relevant documents and receiving the keys to your vehicle.

Required Documents

Accurate and complete documentation is vital for a successful loan application. Lenders need verifiable information to assess your creditworthiness and loan eligibility.

- Proof of Income: Pay stubs, tax returns, or W-2 forms demonstrating your consistent income. This provides evidence of your ability to repay the loan.

- Identification: Driver’s license or passport, and Social Security card, to verify your identity.

- Proof of Residence: Utility bills, bank statements, or lease agreements, confirming your current address.

- Credit Report: A credit report to demonstrate your credit history and creditworthiness.

- Vehicle Information: Information about the car, including the vehicle identification number (VIN).

- Down Payment Documentation: If applicable, documentation of the down payment source.

Importance of Accurate Information

Providing accurate information throughout the application process is essential. Inaccurate information can lead to delays, denial of the loan, or even potential legal issues.

Providing accurate information is critical for a smooth and timely loan process.

Loan Application Deadlines and Processing Times

Processing times and deadlines vary depending on the lender and the complexity of the application. Planning accordingly ensures a timely approval.

| Step | Estimated Timeframe | Possible Deadline |

|---|---|---|

| Initial Inquiry | 1-2 business days | Within a week of car selection |

| Application Submission | 1-3 business days | Within 2 weeks of car selection |

| Credit Check and Evaluation | 3-5 business days | Within 3 weeks of car selection |

| Loan Approval/Denial | 1-2 business days | Within 4 weeks of car selection |

| Funding and Closing | 1-2 business days | Within 5 weeks of car selection |

Loan Terms and Conditions

Understanding the terms and conditions of a 36-month used car loan is crucial for making informed financial decisions. This section delves into key aspects of such loans, including monthly payments, prepayment penalties, and the potential consequences of missed payments. Accurate calculation of the total loan cost is also essential for a clear picture of the overall financial commitment.

Key Terms of a 36-Month Used Car Loan

Loan agreements for used cars typically specify the principal amount borrowed, the interest rate, the loan term (36 months in this case), and the repayment schedule. Other crucial details include the loan origination fee, any additional fees, and the contact information of the lender. These terms are fundamental to understanding the financial obligations associated with the loan.

Monthly Payments

Monthly payments are calculated based on the principal amount, interest rate, and loan term. This involves a complex calculation, typically determined by an amortization schedule. Understanding this calculation is important for budgeting and financial planning.

A common method for calculating monthly payments involves using a formula that takes into account the principal, interest rate, and loan term. The formula considers the time value of money and the interest accrued over the loan’s life. This calculation ensures that the borrower repays the principal and interest in equal monthly installments.

For example, a $15,000 loan with a 6% interest rate over 36 months might result in a monthly payment of approximately $460. Variations in interest rates, loan amounts, and loan terms will affect the exact monthly payment amount.

Prepayment Penalties

Prepayment penalties are fees charged if the loan is repaid before the agreed-upon term. These penalties vary significantly between lenders and loan types. Some loans may have no prepayment penalties, while others might have substantial ones.

It’s crucial to review the loan agreement carefully to understand the terms of any prepayment penalties.

Understanding these penalties in advance allows borrowers to make informed decisions about their repayment strategy.

Consequences of Missing Loan Payments

Missing loan payments can have serious consequences, including late fees, damage to credit scores, and potential legal action. Late fees are added to the outstanding balance, increasing the overall cost of the loan.

A missed payment can trigger a chain of events, negatively impacting the borrower’s financial health.

Furthermore, consistent missed payments can result in a default on the loan, leading to a significant negative impact on credit history.

Calculating the Total Loan Cost Over 36 Months

The total loan cost encompasses the principal amount, accumulated interest, and any additional fees. To calculate this, one must consider the compounding effect of interest over the loan term.

Total loan cost = Principal + Total Interest + Fees.

For instance, a $15,000 loan with a 6% interest rate over 36 months might have a total cost exceeding $17,000, depending on any additional fees. Careful consideration of the total loan cost is vital for making sound financial decisions.

Comparing Different Loan Offers

Securing the best possible loan for your used car involves a crucial step: comparing offers from various lenders. This process allows you to identify the most advantageous terms and conditions, ensuring you get the most value for your money. A well-informed comparison will help you avoid overpaying and maximize your financial savings.

Interest Rate Comparison

Different lenders have varying interest rates for similar loan terms. Understanding these differences is essential for maximizing your savings. Factors like credit score, loan amount, and the lender’s specific policies influence the interest rate offered. A higher credit score, for example, usually results in a lower interest rate.

Loan Options for Used Cars

Numerous loan options cater to used car purchases. These options differ in terms of loan terms, interest rates, and associated fees. Some lenders offer special financing options, while others may have specific requirements for the used car’s condition or the buyer’s credit history. These variations in loan options can significantly impact your monthly payments and overall loan cost.

Importance of Comparing Loan Terms

Comparing loan terms is crucial for making an informed decision. Terms such as loan amount, interest rate, loan duration, and any associated fees should be meticulously reviewed. The loan term directly affects the monthly payment amount. A longer loan term might lead to lower monthly payments but increases the overall interest paid over the loan’s life. Understanding these factors helps you make a financially sound choice.

Effective Loan Offer Comparison

To effectively compare loan offers, gather all relevant information from each lender. Create a structured comparison table, listing interest rates, loan terms, and fees. This organized approach facilitates a side-by-side analysis of each offer. By comparing monthly payments, total interest, and the total cost of the loan, you can make a well-informed decision.

Loan Offer Comparison Table

This table showcases loan offers from three different lenders for a used car with a $15,000 purchase price. Note that the table represents hypothetical data for illustrative purposes only.

| Lender | Interest Rate (%) | Loan Term (Months) | Monthly Payment | Total Interest |

|---|---|---|---|---|

| First National Bank | 6.5 | 36 | $475 | $1,125 |

| Second City Credit Union | 7.0 | 36 | $490 | $1,300 |

| United Auto Finance | 6.0 | 36 | $450 | $900 |

Note: The figures presented in the table are examples and may vary based on individual circumstances. Always verify the exact details with the lender directly.

Refinancing Options

Refinancing a 36-month used car loan can be a strategic move to potentially lower your monthly payments and save money over the life of the loan. Understanding the options, benefits, and costs associated with refinancing is crucial for making an informed decision. This section details refinancing options, clarifies how to determine if refinancing is advantageous, Artikels the procedures involved, and highlights the associated advantages and disadvantages. Careful consideration of these factors can lead to a more financially sound automotive financing strategy.

Determining Refinancing Benefits

Assessing the potential benefits of refinancing involves a comparative analysis of current and potential loan terms. A crucial factor is the current interest rate. If the prevailing interest rates have fallen since the original loan was secured, refinancing can lead to a lower monthly payment and a reduction in total interest paid over the loan term. A comprehensive comparison of the existing loan terms with current market rates, considering factors like credit score and loan terms, will help determine if refinancing is financially viable. A lender’s financial assessment of the borrower’s credit history is critical in determining their eligibility and the terms offered.

Refinancing Procedures

The refinancing process typically involves submitting a new loan application with a different lender. The application process mirrors that of an initial loan application, often requiring similar documentation, such as proof of income, identification, and details of the existing car loan. Once the new loan application is processed, a lender evaluates the applicant’s creditworthiness. A lender will typically review the current loan’s terms, the applicant’s credit score and history, and income stability. The approval process usually involves a thorough assessment of these factors. If approved, the lender will transfer the loan funds to the original lender, discharging the existing loan.

Advantages of Refinancing

Refinancing a used car loan can offer significant advantages. Lower monthly payments can free up budget funds for other needs. A reduction in the total interest paid over the loan term can lead to substantial savings over the life of the loan. This could be illustrated by a scenario where an individual refinancing a $20,000 loan with a lower interest rate sees a reduction of $1,000 in total interest paid. This financial gain can be substantial over the loan’s duration.

- Reduced monthly payments: Lower monthly payments can significantly improve cash flow and financial flexibility.

- Lower total interest paid: Refiancing with a lower interest rate can lead to substantial savings over the life of the loan, often reducing the overall cost of borrowing.

- Improved credit utilization: Refinancing can improve credit utilization ratios if the new loan amount is lower than the outstanding balance on the previous loan, improving the borrower’s credit score and future loan eligibility.

Disadvantages of Refinancing

While refinancing offers numerous potential advantages, there are potential drawbacks. Closing costs and fees associated with the refinancing process may offset some of the savings, and in certain circumstances, these fees could exceed the savings. Additionally, there’s a potential for the application process to take time, which might be a concern if the borrower needs quick access to funds. Finally, refinancing could require the borrower to sign a new loan agreement, and a comprehensive review of the new terms and conditions is essential to ensure they align with the borrower’s needs.

- Closing costs and fees: Refinancing often incurs fees, including application fees, appraisal fees, and origination fees, which can reduce the net savings.

- Potential for loan application delays: The application process can take time, which may be inconvenient if the borrower requires immediate access to funds.

- New loan terms and conditions: A new loan agreement is required, and it is essential to thoroughly review the new terms and conditions to ensure they meet the borrower’s needs.

Costs Associated with Refinancing

| Cost | Description | Example |

|---|---|---|

| Application fee | Fee charged for processing the application. | $50-$100 |

| Origination fee | Fee charged for originating the loan. | 0.5%-1% of the loan amount |

| Closing costs | Fees for closing the new loan, including title and transfer fees. | $100-$500 |

| Prepayment penalty (if applicable) | Penalty for paying off the loan early. | Variable, based on loan terms. |

The costs associated with refinancing can vary significantly depending on the lender, loan terms, and the borrower’s individual circumstances. Thorough research and comparison shopping are crucial to identify the most favorable refinancing options.

Budgeting and Affordability

Securing a used car loan requires careful consideration of your financial situation. A comprehensive budget is crucial to determine if the loan’s monthly payments and associated costs align with your current financial capacity. Understanding your affordability ensures you don’t overextend your budget and maintain financial stability.

Creating a Budget for a 36-Month Loan

A well-structured budget is the cornerstone of responsible financial management. It provides a clear picture of your income and expenses, allowing you to track your spending and identify areas where you can save. This process is particularly important when considering a 36-month used car loan. A budget should be tailored to your specific financial situation and include all anticipated expenses.

Calculating Monthly Payments and Other Costs

Accurate calculation of monthly payments is essential. The loan’s interest rate, principal amount, and loan term directly influence the monthly payment. Tools like online calculators can assist in this process. Beyond the monthly payment, factor in insurance premiums, potential maintenance costs, fuel expenses, and any other associated costs.

Importance of Affordability in Loan Selection

Affordability analysis is critical in the loan selection process. This assessment should consider your current income, existing debts, and anticipated future expenses. An affordable loan ensures that the monthly payments do not strain your budget or jeopardize your financial well-being.

Assessing Loan Affordability

Several factors contribute to assessing loan affordability. A key aspect is comparing the proposed monthly payment to your current disposable income. Consider your savings capacity and emergency fund. An affordable loan should not compromise your ability to meet essential living expenses and maintain a healthy financial cushion.

Sample Budget Template Incorporating a 36-Month Car Loan

A well-organized budget template is beneficial in assessing loan affordability. The template should include sections for income, fixed expenses (housing, utilities, etc.), variable expenses (groceries, entertainment), and debt payments. A dedicated section for the 36-month car loan’s monthly payment should be included. An example below Artikels a potential structure:

| Category | Description | Amount |

|---|---|---|

| Income | Salary | $4,000 |

| Fixed Expenses | Rent | $1,200 |

| Fixed Expenses | Utilities | $200 |

| Variable Expenses | Groceries | $300 |

| Variable Expenses | Transportation | $150 |

| Debt Payments | Credit Card | $200 |

| Loan Payments | 36-month Car Loan | $400 |

| Savings | Emergency Fund | $100 |

| Total Expenses | $2,550 | |

| Available Funds | $1,450 |

Monthly payments for a 36-month loan should ideally fall within the range of 20-35% of your gross monthly income to ensure financial stability.

Consumer Protection and Rights

Understanding your rights as a borrower is crucial when taking out a used car loan. Knowing your rights and protections can empower you to make informed decisions and navigate potential issues effectively. This section details consumer rights, safeguards against scams, and essential steps for resolving disputes.

Consumer Rights Related to Used Car Loans

Used car loan agreements are governed by consumer protection laws designed to ensure fair treatment for borrowers. These laws typically Artikel the rights of consumers, including the right to accurate information about the loan terms, the right to a clear and concise loan agreement, and the right to a fair and transparent interest rate. Consumers have the right to dispute errors or inaccuracies in their loan documents and demand corrections. They are also entitled to receive explanations regarding any fees or charges associated with the loan.

Protecting Yourself from Loan Scams

Loan scams are unfortunately prevalent. Be highly cautious of unsolicited loan offers, particularly those promising exceptionally low interest rates or extremely quick approvals. Verify the legitimacy of any lender by researching their reputation and credentials. Avoid sharing sensitive financial information with unknown entities. Legitimate lenders will not ask for personal details via email or text. Always contact the lender directly to confirm the authenticity of the loan offer and any associated fees.

Understanding Your Loan Agreement

Thoroughly reviewing the loan agreement before signing is essential. Pay close attention to details like the interest rate, fees, repayment schedule, and any prepayment penalties. Don’t hesitate to ask questions about any clauses or terms that are unclear. A clear understanding of the agreement will prevent misunderstandings and potential issues down the road. Seek professional advice if needed to interpret complex terms.

Resolving Loan Disputes

Disputes regarding used car loans may arise, but they can often be resolved through communication and adherence to established procedures. Start by documenting all communications with the lender. If initial attempts at resolution fail, consider contacting consumer protection agencies for assistance. Mediation or arbitration may be options to facilitate a mutually agreeable solution. Understanding the lender’s dispute resolution policy and procedures is crucial.

Consumer Protection Agencies Related to Loans

Several consumer protection agencies oversee financial institutions and provide resources for resolving loan disputes. These agencies can provide information on consumer rights, assist with complaints, and mediate disputes between consumers and lenders.

- Federal Trade Commission (FTC): The FTC is a vital resource for consumers facing various financial issues, including loan disputes. Their website provides information on identifying and avoiding scams, resolving complaints, and understanding consumer rights.

- Consumer Financial Protection Bureau (CFPB): The CFPB is a key regulatory body focused on protecting consumers in financial transactions. Their website offers resources and guidance for consumers regarding loans, credit, and other financial products.

- State Attorneys General Offices: Each state has an attorney general’s office responsible for consumer protection. These offices often handle complaints and provide guidance regarding specific state laws relating to consumer protection.