Understanding Used Car Refinancing

Used car refinancing allows you to secure a new loan for your existing used car, potentially at a better interest rate or terms than your current loan. This can save you money on interest payments over the life of the loan. It’s a strategic financial tool to potentially reduce your monthly payments and overall cost of ownership.

Refinancing a used car loan isn’t just about finding a lower interest rate; it’s about evaluating the terms of your existing loan and comparing them to new loan options. Understanding the process and potential benefits can help you make an informed decision about your financial future.

Used Car Refinancing Options

Different refinancing options cater to various financial needs and circumstances. Exploring these options is key to finding the best fit for your situation. Factors like credit score, loan amount, and the remaining loan term influence the most suitable option.

- Traditional Bank Refinancing: This involves applying to a traditional bank or credit union for a new loan to replace your current one. This method often requires a thorough credit check and may involve application fees. It can provide competitive rates, but the application process can take time. For example, a borrower with excellent credit may secure a lower interest rate from a traditional bank compared to a subprime lender.

- Online Refinancing: Online lenders offer convenient and fast refinancing options. These lenders frequently use an online platform for applications and approvals. They often have a streamlined process but may have higher interest rates than traditional banks, particularly for borrowers with less-than-perfect credit. For example, a borrower with a recent credit score dip may find favorable terms with an online lender specializing in subprime loans.

- Private Lender Refinancing: Private lenders, such as individuals or companies, offer loans directly to borrowers. This method might provide faster approvals and potentially lower rates for those with good credit and a strong financial history. However, the lack of regulatory oversight can make it a riskier choice. For example, a borrower with a solid credit history and a proven repayment record might find better rates and terms with a private lender than with a traditional bank.

Benefits of Refinancing a Used Car Loan

Refinancing a used car loan can offer numerous advantages, potentially leading to significant savings. Careful consideration of these benefits can influence your decision to refinance.

- Lower Interest Rates: A primary benefit is the potential to secure a lower interest rate on your new loan compared to your existing one. This directly translates to lower monthly payments and a lower total cost of borrowing over the life of the loan.

- Lower Monthly Payments: Refinancing can lead to lower monthly payments, which can significantly impact your budget and financial stability. This is especially valuable if you are experiencing financial hardship or want to free up more cash flow.

- Improved Loan Terms: Refinancing often provides the opportunity to adjust the loan term. A shorter term can reduce the overall interest paid, while a longer term might be beneficial for borrowers seeking more manageable monthly payments.

Reasons for Refinancing a Used Car Loan

Several factors can motivate someone to refinance their used car loan. Recognizing these reasons can help in assessing the need for refinancing.

- Lower Interest Rates: A primary driver for refinancing is the pursuit of a lower interest rate on the new loan, potentially leading to substantial savings over the loan’s life. A lower interest rate directly reduces monthly payments and total interest paid.

- Improved Credit Score: A better credit score can sometimes qualify a borrower for better interest rates and terms, thus justifying the effort of refinancing.

- Financial Hardship: Facing financial difficulties can make a refinance advantageous, as it can potentially reduce monthly payments and provide some relief from debt pressures.

Comparison of Refinancing Options

The following table compares and contrasts different used car refinancing options:

| Option | Description | Pros | Cons |

|---|---|---|---|

| Traditional Bank Refinancing | Applying to a bank or credit union for a new loan. | Competitive rates, established lender, regulatory oversight. | Potential lengthy application process, credit check requirement. |

| Online Refinancing | Applying for a loan through an online lender. | Convenient, fast application process, potential for faster approvals. | Potentially higher interest rates, limited personal interaction. |

| Private Lender Refinancing | Applying for a loan from an individual or company. | Potentially faster approvals, potentially lower rates for high-credit borrowers. | Lack of regulatory oversight, higher risk, potential for scams. |

Factors Affecting Refinancing Rates

Used car refinancing rates are influenced by a complex interplay of market forces and individual borrower characteristics. Understanding these factors is crucial for borrowers seeking the most favorable terms. Knowing what impacts your rate allows you to make informed decisions and potentially save money.

Credit Score Impact

A strong credit score is a significant factor in determining refinance rates. Lenders use credit scores to assess the risk associated with lending you money. A higher credit score indicates a lower risk of default, allowing lenders to offer more favorable interest rates. Conversely, a lower credit score signifies a higher risk, leading to higher interest rates. This is because lenders need to compensate for the increased likelihood of not receiving the full amount of the loan back. Credit scores are crucial in the car financing process as they directly correlate with the interest rates offered.

Interest Rate Environment Influence

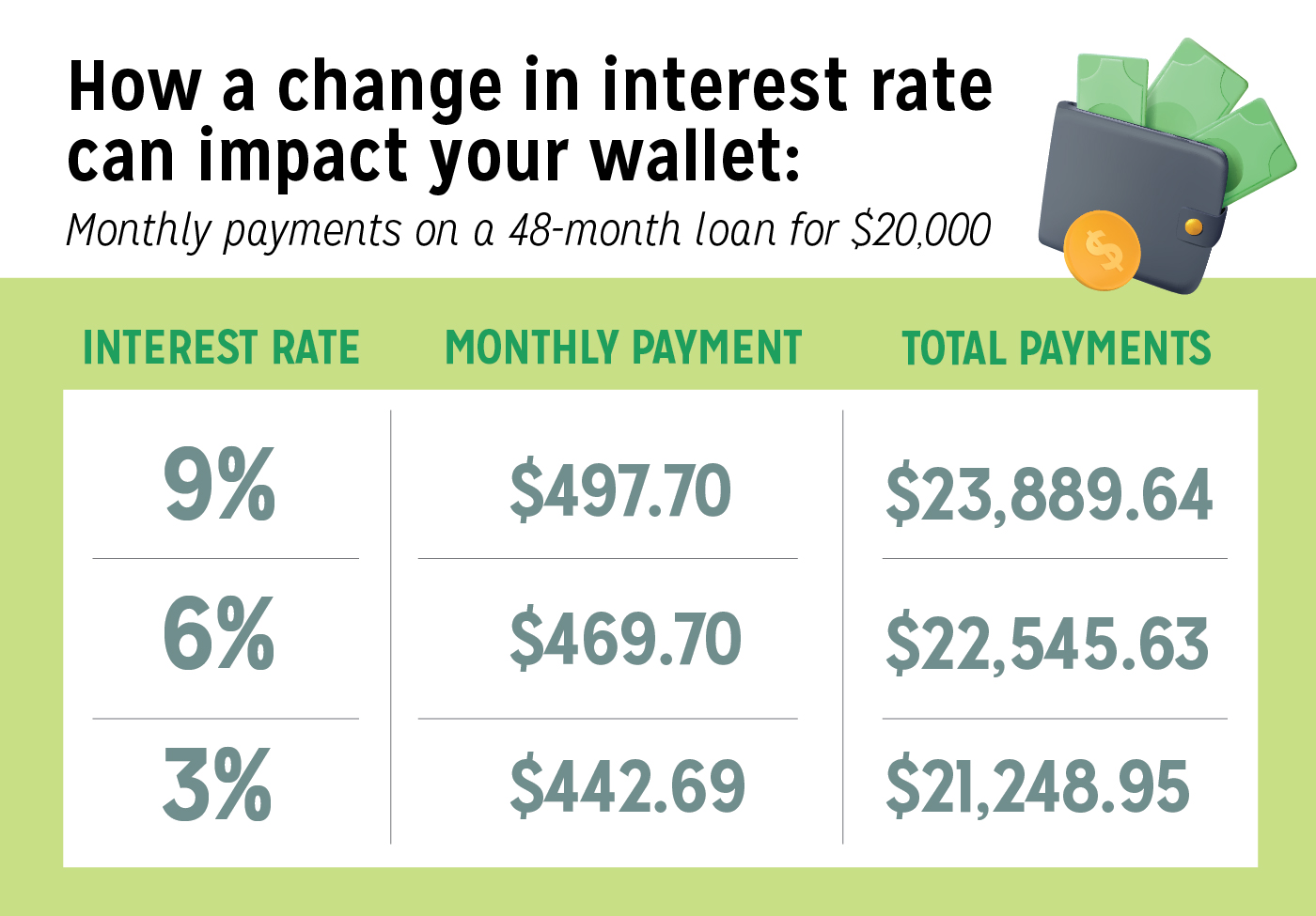

The overall interest rate environment significantly impacts used car refinance rates. When general interest rates rise, refinancing rates tend to rise as well. This is because lenders need to maintain profitability and competitive rates in the prevailing market conditions. Conversely, falling interest rates often lead to lower refinance rates. The Federal Reserve’s monetary policy decisions are key drivers in the interest rate environment. For example, during periods of economic uncertainty or inflation, interest rates tend to increase, making refinancing more expensive.

Loan Terms Impact

Loan terms, including the loan amount and loan duration, also play a role in determining refinance rates. Generally, larger loan amounts translate to higher rates due to increased risk for the lender. Similarly, longer loan terms often result in higher rates as the lender assumes risk over a more extended period. This is because the lender has to manage the loan for a longer period, potentially increasing the risk of losses due to factors like unexpected economic shifts or borrower defaults. A shorter loan duration can lead to lower rates as the risk is reduced for the lender. For instance, a $10,000 loan with a 36-month term might have a lower rate than a $15,000 loan with a 60-month term, assuming all other factors remain constant.

Illustrative Impact of Credit Scores on Rates

| Credit Score | Estimated Rate | Impact Explanation |

|---|---|---|

| 700 | 4.5% | Good credit scores usually lead to lower rates, reflecting lower risk for the lender. |

| 650 | 5.5% | Lower credit scores result in higher rates, indicating a higher risk for the lender. |

| 600 | 6.5% | Very low credit scores often result in higher rates, requiring lenders to compensate for the increased risk. |

Comparing Refinancing Offers

Navigating the landscape of used car refinance offers can feel overwhelming. Understanding how to compare different options is crucial for securing the best possible rate and terms. A methodical approach, coupled with a clear understanding of the key factors involved, will empower you to make an informed decision.

Comparing refinance offers requires a structured approach that goes beyond simply looking at interest rates. This involves evaluating the complete financial package, considering hidden fees, and analyzing the long-term implications of different loan terms. A well-defined comparison process allows you to identify the most favorable offer.

Methods for Comparing Refinancing Offers

A systematic approach to comparing refinance offers involves several key steps. First, gather all available offers from various lenders. Then, use a standardized comparison method to evaluate the offers based on crucial factors.

Template for Recording Key Offer Details

A standardized template is essential for effectively recording and comparing refinance offers. This template should include key details like the lender’s name, interest rate, loan fees, loan term, and any additional charges. This structured format facilitates a clear comparison of the various offers.

| Lender | Interest Rate | Fees | Loan Term |

|---|---|---|---|

| Lender A | 4.75% | $150 | 60 months |

| Lender B | 4.50% | $100 | 72 months |

| Lender C | 4.60% | $125 | 66 months |

Factors to Consider When Evaluating Refinancing Offers

Evaluating refinance offers involves more than just the interest rate. Consider the following factors:

- Interest Rate: The annual percentage rate (APR) is a critical factor. Compare the interest rates offered by different lenders, considering the APR as a comprehensive measure of the cost of borrowing.

- Loan Fees: Explore the associated fees, including origination fees, application fees, and prepayment penalties. These fees can significantly impact the overall cost of the loan.

- Loan Term: A longer loan term typically results in lower monthly payments but a higher total interest paid over the life of the loan. A shorter term has higher monthly payments but lower total interest paid. The optimal loan term depends on your individual financial situation and budget.

- Total Cost of the Loan: Calculate the total cost of the loan by considering not only the interest rate but also any associated fees. This will give a clear picture of the true cost of borrowing.

- Additional Charges: Be mindful of any additional charges, such as late payment fees, prepayment penalties, or balloon payments, that could significantly impact the overall cost of the loan.

Comparing and Contrasting Multiple Refinancing Offers

Comparing multiple refinance offers requires careful analysis of each offer’s individual components. By creating a table or spreadsheet to record the key details, you can systematically compare the interest rates, fees, and loan terms offered by each lender. This allows you to make an informed decision based on the specific details of each offer.

Organizing a Table to Compare Refinancing Offers

A well-structured table allows for easy comparison of different refinance offers. The table should include columns for lender, interest rate, fees, loan term, and any other relevant details. This structured format will facilitate the identification of the most advantageous offer.

Refinancing Alternatives and Considerations

Beyond traditional refinancing options, several alternative financing avenues exist for used car purchases. Understanding these alternatives allows you to make an informed decision, considering the specific circumstances of your financial situation and future goals. This exploration delves into the pros and cons of each option, highlighting the potential implications of your choice on your overall financial health.

Evaluating refinancing options alongside other financing avenues provides a broader perspective on your available choices. This comprehensive analysis considers factors beyond just the interest rate, encompassing the terms, fees, and potential long-term effects on your budget.

Alternative Financing Options

Various alternative financing options are available for used car purchases, each with its own set of benefits and drawbacks. These options can include personal loans, dealer financing, or even using savings or a line of credit. Understanding the unique characteristics of each alternative is crucial to making an informed decision.

- Personal Loans: Personal loans can offer competitive interest rates, often lower than dealer financing. However, qualifying for a personal loan can be challenging, requiring a good credit score and a thorough loan application process. The repayment terms and potential fees associated with personal loans should be carefully considered. For example, a borrower with a high credit score and a strong repayment history might secure a lower interest rate on a personal loan compared to dealer financing.

- Dealer Financing: Dealer financing is a common option offered directly by the dealership. The terms and interest rates can vary significantly based on the dealership and your credit history. While it often involves a streamlined application process, the interest rates might not be as competitive as those available through other lenders. Be wary of hidden fees and ensure you fully understand the terms before signing any loan documents.

- Using Savings or a Line of Credit: If you have sufficient savings, using these funds to finance a used car purchase can offer immediate access to capital without the need for a loan application. However, this approach may impact your ability to achieve other financial goals or may expose you to higher interest rates if your savings are used to pay interest on other debts. Furthermore, the flexibility of a line of credit might make it attractive, but it’s essential to understand the interest rates and potential fees before making a decision.

Implications of Choosing a Specific Option

The choice of a specific refinancing or alternative financing option carries significant implications for future financial decisions. Understanding these implications will help you align your financial strategies with your long-term goals.

- Impact on Credit Score: Each financing option impacts your credit report differently. A personal loan, for instance, can impact your credit utilization ratio and overall credit history, while dealer financing typically involves reporting to credit bureaus.

- Long-Term Financial Planning: The selected financing option can influence your long-term financial planning, including budget allocation, savings strategies, and debt management plans. Choosing a loan with a high interest rate might impact your ability to save or invest for future goals.

- Comparison of Advantages and Disadvantages: Each financing option offers different advantages and disadvantages. Personal loans often provide lower interest rates but can be more difficult to secure. Dealer financing might be easier to obtain but may come with higher interest rates. Using savings or a line of credit offers immediate access to funds but could impact other financial goals. A comparative analysis is essential to make an informed decision.

Tips for a Successful Refinancing

Securing a favorable used car refinance hinges on meticulous preparation and strategic negotiation. Understanding the process and key factors involved empowers you to secure the best possible terms. This section provides actionable strategies to maximize your chances of success.

Preparing for Refinancing

Thorough preparation is paramount to a smooth and successful refinancing process. This involves assembling all necessary documentation and understanding your current financial situation. A clear understanding of your current loan terms, including interest rates and remaining loan balance, is essential. Gathering this information allows you to evaluate your options and negotiate effectively. Additionally, reviewing your credit report and score prior to the application process is crucial to understanding any areas for improvement.

Negotiating Favorable Rates

Negotiation plays a significant role in securing a competitive interest rate. Demonstrating financial responsibility and understanding the current market rates empowers you to advocate for a favorable deal. A pre-approval from a lender, coupled with a strong understanding of the current market rates, puts you in a stronger position during negotiations. Presenting a compelling case for your creditworthiness, coupled with the lender’s willingness to offer a competitive rate, can lead to a successful outcome.

Shopping Around for the Best Rates

Comparison shopping is essential for finding the most competitive used car refinance rates. Don’t limit yourself to one or two lenders. Extensive research and comparing offers from various lenders is crucial to securing the most attractive terms. Seeking quotes from multiple lenders allows you to evaluate interest rates, fees, and terms. This proactive approach ensures you gain access to a wide range of options, maximizing your chances of securing the best rate.

Maintaining Good Credit

Maintaining a strong credit history is vital for securing lower interest rates. Regular payments, timely bill management, and responsible credit utilization contribute to a positive credit score. Avoiding unnecessary credit inquiries and ensuring that your credit utilization ratio remains low helps maintain a favorable credit score. Lenders often use credit scores to assess your risk, making good credit a key factor in securing a competitive rate.

Contacting Lenders and Obtaining Quotes

Contacting lenders and obtaining quotes is a crucial step in the refinancing process. Utilizing online tools and directly contacting lenders allows for streamlined communication and efficient comparisons. Requesting detailed quotes and comparing interest rates, fees, and terms is critical to making informed decisions. Comparing the various terms offered by different lenders, including the interest rate, loan term, and any additional fees, will ensure you select the best option. This process ensures you make an informed decision based on the available options.