Overview of Navy Federal Used Car Rates

Navy Federal Credit Union offers used car loan programs tailored to its members, often with competitive interest rates. These programs aim to provide accessible financing options for a variety of vehicles. Understanding the specifics of these loans is crucial for making informed decisions.

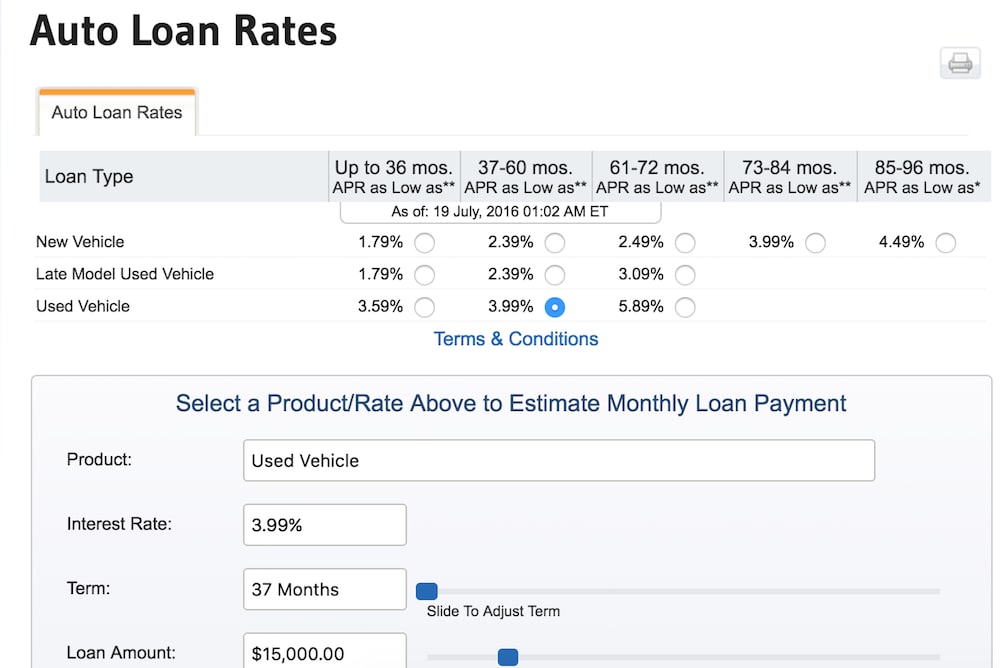

Used car loans through Navy Federal are designed to help members acquire pre-owned vehicles. The terms and conditions, along with the interest rates, vary depending on individual circumstances and the specifics of each loan application. Navy Federal’s used car loan programs cater to a diverse range of vehicles, from economical compact cars to larger SUVs and trucks.

Types of Vehicles Financed

Navy Federal’s used car loan programs generally cover a broad spectrum of pre-owned vehicles. This includes passenger cars, trucks, SUVs, and vans. The types of vehicles often considered are those that meet the general standards and specifications of the loan program. Factors like vehicle age, mileage, and condition play a significant role in the approval process.

Eligibility Criteria

Navy Federal’s used car loan eligibility criteria are designed to ensure the loan program is responsible. Key aspects include the applicant’s credit history, income, and overall financial standing. Membership in Navy Federal is often a significant factor in the eligibility process. Additionally, the applicant’s debt-to-income ratio is a common consideration.

Factors Influencing Interest Rates

Several factors influence the interest rate for a used car loan at Navy Federal. These factors include the applicant’s credit score, the loan amount, the vehicle’s age and condition, and the prevailing market interest rates. A higher credit score generally translates to a lower interest rate. The loan amount also plays a role, with larger loans potentially resulting in higher rates.

Key Terms in Used Car Loans

| Term | Definition |

|---|---|

| Loan Amount | The total sum of money borrowed to purchase the vehicle. |

| Interest Rate | The percentage charged on the loan amount over a period. |

| Loan Term | The duration over which the loan is to be repaid. |

| Monthly Payment | The fixed amount paid each month to repay the loan. |

| Down Payment | The upfront payment made by the borrower towards the vehicle’s purchase price. |

| Credit Score | A numerical representation of a borrower’s creditworthiness, affecting interest rates. |

| Vehicle Appraisal | An assessment of the vehicle’s value, determining the loan amount. |

Comparison of Rates with Other Lenders

Navy Federal’s used car loan rates are often competitive, but they aren’t always the best option. Understanding how Navy Federal rates stack up against other lenders is crucial for securing the most favorable terms. Factors like credit score, loan amount, and the vehicle’s condition will influence the final rate offered by any lender.

Comparing rates requires a careful consideration of not just the interest rate, but also associated fees, loan terms, and any other conditions. A lender’s reputation and customer service are also important factors. This analysis will highlight how Navy Federal rates measure up to other major lenders, helping you make an informed decision.

Factors Affecting Used Car Loan Rates

Several key factors influence the interest rate a lender offers. Credit score is a major determinant, with higher scores typically leading to lower rates. The loan amount plays a role; larger loans might carry higher rates. The vehicle’s condition, age, and mileage will also impact the perceived risk for the lender. These factors, alongside the current market conditions and the lender’s specific lending policies, determine the final rate offered.

Comparison Table of Used Car Loan Rates

This table provides a simplified comparison of potential rates from various lenders. Keep in mind that these are illustrative examples, and actual rates will vary based on individual circumstances.

| Lender | Interest Rate (Example) | Fees (Example) | Other Terms (Example) |

|---|---|---|---|

| Navy Federal Credit Union | 4.5% | Documentation fee: $100, Origination fee: $200 | Loan terms: 36-72 months, Prepayment penalties may apply |

| Major Bank (Example) | 5.2% | Documentation fee: $150, Origination fee: $300 | Loan terms: 36-60 months, Prepayment penalties may apply |

| Large Credit Union (Example) | 4.8% | Documentation fee: $125, Origination fee: $250 | Loan terms: 36-72 months, Prepayment penalties may apply |

| Online Lender (Example) | 5.0% | No documentation fee, Origination fee: $250 | Loan terms: 36-60 months, Prepayment penalties may apply |

Calculating Total Loan Cost

The total cost of a used car loan extends beyond the interest rate. It’s essential to consider all fees and charges to get a complete picture. A simple calculation is illustrated below:

Loan Amount: $10,000

Interest Rate: 5%

Loan Term: 60 months

Monthly Payment: $197.25

Total Interest Paid: $1,222.28

This calculation demonstrates that the total cost exceeds the principal loan amount by the total interest paid over the loan term. Detailed calculations should always be performed for an accurate assessment of the true cost of borrowing.

Impact of Credit Score on Rates

Navy Federal Credit Union, like most lenders, uses credit scores to assess risk and determine the interest rates for used car loans. A higher credit score generally translates to a lower interest rate, as it signifies a lower risk of default. This is because lenders view borrowers with strong credit histories as more reliable in repaying their loans. Understanding how credit scores affect your loan terms is crucial for securing the most favorable financing options.

Creditworthiness significantly influences the terms of a used car loan at Navy Federal. A borrower with a strong credit history will likely qualify for a lower interest rate and a longer loan term, often leading to lower monthly payments. Conversely, a borrower with a weaker credit history might face a higher interest rate and a shorter loan term, potentially resulting in higher monthly payments. The relationship between creditworthiness and loan terms is directly proportional, reflecting the lender’s risk assessment.

Credit Score and Interest Rate Variations

Credit scores play a pivotal role in determining the interest rate for a used car loan at Navy Federal. A higher credit score generally leads to more favorable loan terms, including lower interest rates and potentially longer loan durations. The following table illustrates potential rate differences based on various credit score ranges. Note that these are estimates, and actual rates may vary based on individual circumstances, such as the vehicle’s condition, loan amount, and other factors.

| Credit Score Range | Estimated Interest Rate |

|---|---|

| 680-719 | 5.50% – 7.50% |

| 720-759 | 4.50% – 6.50% |

| 760-799 | 3.50% – 5.50% |

| 800+ | 2.50% – 4.50% |

A borrower with a credit score of 750 or above is typically eligible for a lower interest rate compared to a borrower with a score below 700.

These estimated interest rates represent a general guideline. Factors such as the vehicle’s make, model, and condition, and the specific loan terms, could also affect the final rate. For instance, a loan for a newer, higher-value vehicle might result in a lower interest rate than a loan for an older, lower-value vehicle, even if the credit scores are the same. This underscores the multifaceted nature of loan rate determination.

Factors Affecting Interest Rates

Used car loan interest rates are influenced by a complex interplay of economic conditions, vehicle characteristics, and borrower profiles. Understanding these factors is crucial for borrowers to make informed decisions when financing their used vehicle purchases. Navy Federal, like other lenders, carefully considers these elements to determine the appropriate interest rate for each loan application.

Several key factors significantly impact the interest rates charged on used car loans. These factors, from the overall economic climate to the specific details of the vehicle itself, are meticulously assessed by lenders to ensure responsible lending practices and to manage risk effectively.

Impact of the Current Economic Climate

The current economic environment plays a significant role in shaping used car loan interest rates. Factors such as inflation, unemployment rates, and overall economic growth influence the availability and cost of credit. For instance, during periods of high inflation, lenders may increase interest rates to mitigate potential losses. Conversely, a robust economy might lead to lower interest rates as the overall demand for credit decreases. The Federal Reserve’s monetary policy decisions, designed to manage inflation and economic growth, directly impact the cost of borrowing across all sectors, including used car loans.

Vehicle Condition, Mileage, and Model Year

The condition, mileage, and model year of a used vehicle directly correlate with its perceived value and residual worth. A vehicle in excellent condition with low mileage and a more recent model year is generally perceived as having a higher resale value and lower risk for the lender. This translates into a potentially lower interest rate for the borrower. Conversely, a vehicle with significant damage, high mileage, or an older model year will likely command a higher interest rate due to the increased risk associated with its potential future value and repairability. Lenders carefully evaluate these factors to assess the potential risk of the loan.

Additional Factors Influencing Used Car Loan Rates

Beyond the economic climate and vehicle specifics, several other factors influence used car loan interest rates. These include the borrower’s credit history, the loan amount, and the length of the loan term. A borrower with a strong credit history and a low debt-to-income ratio will likely qualify for a lower interest rate compared to a borrower with a less favorable credit profile. The loan amount itself can also influence the interest rate, as larger loans often come with higher rates due to increased risk for the lender. Similarly, a longer loan term typically results in a higher interest rate compared to a shorter term.

- Credit Score: A higher credit score typically translates to a lower interest rate, reflecting the borrower’s lower risk profile. Conversely, a lower credit score may lead to a higher interest rate due to the increased risk associated with potential loan defaults.

- Loan Amount: Larger loan amounts often come with higher interest rates because they represent a greater financial risk for the lender.

- Loan Term: Longer loan terms typically result in higher interest rates compared to shorter terms, as the lender assumes a higher risk over a more extended period.

- Down Payment: A larger down payment demonstrates the borrower’s financial commitment to the loan, often leading to a lower interest rate.

- Loan Type: Different types of loans, such as those with specific features or requirements, may carry varying interest rates.

- Market Conditions: Fluctuations in the used car market, such as periods of high demand or low supply, can influence interest rates.

- Vehicle Type: Certain types of vehicles, such as luxury or high-performance models, might command higher interest rates due to their higher value and potential maintenance costs.

Steps to Obtain a Used Car Loan with Navy Federal

Securing a used car loan through Navy Federal involves a structured process designed to ensure a smooth and efficient experience for members. Understanding the steps involved will help you navigate the application process effectively and increase your chances of securing the loan you need.

The application process for a used car loan with Navy Federal is typically straightforward. You’ll need to gather the necessary documentation and complete the application form. Navy Federal’s online platform makes the process convenient and accessible, allowing you to manage your application from the comfort of your home.

Application Requirements

Before initiating the loan application, gathering the necessary documentation is crucial. This will expedite the process and minimize potential delays. Essential documents typically include proof of identity, income verification, and details about the vehicle you wish to purchase.

- Proof of Identity: A valid government-issued photo ID, such as a driver’s license or passport, is required to verify your identity. This document is essential for security and regulatory compliance.

- Proof of Income: Navy Federal will need evidence of your income to assess your ability to repay the loan. This can include pay stubs, tax returns, or bank statements. The frequency and amount of income will be scrutinized to ensure the loan’s affordability.

- Vehicle Information: Accurate details about the vehicle are necessary. This includes the year, make, model, VIN (Vehicle Identification Number), and mileage of the used car. A clear description of the vehicle’s condition, and any recent repairs or maintenance, are also important.

- Loan Application Form: Complete the application form accurately and comprehensively. This form will solicit information regarding your financial status, credit history, and the details of the loan you are seeking.

Loan Approval Process

The loan approval process involves several stages, including a credit check and a review of the submitted documentation. Once you submit the application, Navy Federal will evaluate your financial profile and creditworthiness.

- Credit Check: Navy Federal will perform a credit check to assess your credit history and determine your creditworthiness. This assessment considers your credit score, payment history, and outstanding debts.

- Documentation Review: Your submitted documents are thoroughly reviewed to verify the accuracy of the information provided. Any discrepancies or missing information may necessitate additional documentation.

- Loan Offer: If approved, Navy Federal will provide a loan offer outlining the interest rate, loan terms, and other relevant details. This offer is contingent upon your acceptance.

Timeline for Obtaining a Loan

The timeframe for obtaining a used car loan with Navy Federal can vary depending on several factors. These include the completeness of your application, the complexity of the loan application, and the current workload of the processing department. However, the process is typically expedited with complete documentation.

- Application Submission: Once you submit your application, Navy Federal typically processes it within a few business days.

- Loan Approval: The time it takes for loan approval can vary from a few business days to a couple of weeks, depending on the circumstances.

- Loan Closing: Once you accept the loan offer, the loan closing process can take another few business days.

Step-by-Step Guide to Applying

- Gather all necessary documents: Ensure you have all the required documents, including proof of identity, income verification, and vehicle information.

- Complete the online application: Access the Navy Federal website and complete the online application form accurately and thoroughly.

- Submit the application: Submit the completed application and all supporting documents through the designated channels.

- Review the loan offer: Carefully review the loan offer provided by Navy Federal, including the interest rate and loan terms.

- Accept the loan offer: If you accept the offer, follow the instructions provided by Navy Federal to finalize the loan.

Tips for Negotiating Used Car Rates

Negotiating the price of a used car can feel daunting, but with the right strategies, you can secure a deal that benefits you. Understanding market values and leveraging the loan process are key components of successful negotiation. This section will provide practical tips to help you navigate the complexities of used car purchases and secure the best possible price.

Successfully negotiating a used car price involves a combination of research, strategy, and a bit of assertiveness. Knowing the fair market value of the vehicle, understanding the lender’s role, and having a clear negotiation strategy are crucial for getting the best possible deal. Ultimately, these strategies aim to achieve a price that aligns with the car’s condition, mileage, and market value while considering the loan terms.

Market Research for Fair Prices

Thorough market research is the foundation of a successful negotiation. Knowing the prevailing market value for similar used cars allows you to make informed decisions and confidently present your offer. Utilize online resources, such as Kelley Blue Book (KBB) and Edmunds, to compare the prices of comparable vehicles based on make, model, year, mileage, and condition. Look for used cars with similar specifications advertised in your local area. This comprehensive research will provide a baseline for your negotiation.

Leveraging the Loan Process for Better Deals

The loan process itself can be a powerful tool in your negotiation arsenal. If you have pre-approval for a loan from Navy Federal or another lender, you’ll have a significant advantage. Knowing the amount you can borrow gives you a clear budget and enables you to make an offer that is realistic for the lender and the seller. This also allows you to avoid being pressured into accepting a higher price than you are comfortable with.

Negotiation Strategies

A well-defined negotiation strategy can significantly improve your chances of securing a favorable price. These strategies combine research with assertive communication.

- Start with a lower offer: Never start with your desired price. Begin with a price that is lower than your research indicates as a fair market value. This sets the stage for negotiation and demonstrates your willingness to bargain.

- Be prepared to walk away: Having a backup plan is crucial. If the seller is unwilling to negotiate to a reasonable price, be prepared to walk away. This demonstrates your resolve and can encourage the seller to reconsider their position.

- Highlight the car’s flaws: Don’t be afraid to point out any minor imperfections in the car’s condition, but do so constructively. Use this as an opportunity to negotiate a lower price, rather than as a way to discourage the seller.

- Focus on the total cost of ownership: Beyond the initial purchase price, consider the cost of insurance, maintenance, and potential repairs. Highlight these additional costs in your negotiation, emphasizing the total cost of ownership and the importance of a fair price.

- Be polite and respectful: Maintaining a respectful and professional demeanor throughout the negotiation process is essential. A courteous approach can create a positive environment that fosters productive discussions.

- Consider financing options: Inquire about financing options from the seller, as this can sometimes help you secure a lower price. If you have a pre-approved loan, this is particularly valuable.

Illustrative Examples of Rates

Understanding the factors influencing Navy Federal used car loan rates is crucial for prospective borrowers. These examples demonstrate how different credit scores and vehicle types can impact the loan terms. While precise rates depend on individual circumstances, these scenarios provide a valuable insight into the potential range of loan options.

Loan Scenarios with Varying Conditions

This section presents illustrative scenarios to demonstrate how credit score and vehicle type influence Navy Federal used car loan rates. The provided examples are hypothetical and do not represent specific loan offers.

| Scenario | Vehicle | Credit Score | Loan Amount | Interest Rate | Monthly Payment |

|---|---|---|---|---|---|

| Scenario 1: Reliable Sedan | 2018 Honda Civic | 700 | $15,000 | 6.5% | $375.00 |

| Scenario 2: Popular SUV | 2020 Toyota RAV4 | 750 | $20,000 | 5.8% | $450.00 |

| Scenario 3: Luxury Vehicle | 2022 BMW 3 Series | 800 | $30,000 | 4.8% | $725.00 |

| Scenario 4: High-Mileage Truck | 2015 Ford F-150 | 650 | $10,000 | 7.2% | $250.00 |

| Scenario 5: Older Compact Car | 2010 Mazda3 | 680 | $8,000 | 7.8% | $210.00 |

Factors Impacting Calculated Loan Amounts and Interest Rates

The table above showcases a range of loan scenarios, highlighting the impact of creditworthiness and vehicle characteristics. Higher credit scores typically result in lower interest rates and potentially larger loan amounts. The vehicle’s age, mileage, condition, and market value also play a significant role in determining the loan amount and interest rate. For example, a newer, higher-value vehicle often qualifies for a larger loan amount and a lower interest rate compared to an older, lower-value vehicle with higher mileage. The loan amount itself is dependent on the appraised value of the vehicle and the amount the borrower is seeking to finance.

Recent Trends in Used Car Market

The used car market has experienced significant fluctuations in recent years, impacting everything from pricing to loan rates. Understanding these trends is crucial for consumers seeking to purchase a used vehicle, particularly when considering financing options. These dynamics directly influence the interest rates offered by lenders like Navy Federal.

The used car market, historically a reliable source of affordable transportation, has seen dramatic shifts in pricing and availability, impacting loan rates. Factors such as supply chain disruptions, global economic conditions, and consumer demand have combined to create a complex and dynamic environment.

Pricing Fluctuations

Used car prices have exhibited significant volatility in recent years. Periods of high demand, often coinciding with shortages of new cars, have driven used car prices up considerably. Conversely, periods of reduced demand or increased supply have led to price drops. These fluctuations directly affect the affordability and desirability of used cars, and consequently influence the interest rates offered by lenders. For example, in 2021, used car prices reached record highs, and lenders adjusted interest rates accordingly to reflect the increased risk associated with financing these vehicles.

Impact on Loan Rates

The volatility in used car prices directly impacts used car loan rates. When used car prices are high, lenders generally increase interest rates to mitigate the risk of financing vehicles at inflated valuations. Conversely, lower used car prices often correlate with lower interest rates as the risk to the lender diminishes. This dynamic is crucial for consumers seeking financing, as it highlights the importance of understanding current market conditions.

Current Market Conditions

The current market presents a mixed bag for used car buyers. Supply chain issues have eased somewhat, and new car production has increased. This, coupled with a cooling consumer demand, has contributed to a moderate decline in used car prices. However, regional variations persist, and specific vehicle types continue to see price fluctuations. For instance, certain models with limited availability or high demand may still command premium prices.

Influence of Market Changes on Rates

Market changes directly influence used car loan rates. As used car prices moderate, lenders are often adjusting their rates downward. This trend is expected to continue as supply chain issues ease and consumer demand remains stable. However, factors such as unforeseen economic shifts or sudden surges in demand can still impact rates. Lenders continuously evaluate market trends to adjust risk assessments and offer competitive financing options.