Overview of Used Car Interest Rates in 2025

Used car interest rates in 2025 are projected to exhibit a dynamic pattern, influenced by the interplay of economic factors and market conditions. While a precise prediction is impossible, several trends suggest potential shifts from previous years. The prevailing economic climate will significantly impact the availability and cost of credit, influencing the rates consumers face when financing their used car purchases.

The general economic climate in 2025 is anticipated to be one of moderate growth, with inflation remaining a key concern. This balance of factors will likely lead to interest rates that are somewhat elevated compared to the historically low rates seen during the pandemic era, but potentially lower than the highs experienced in certain periods. This is particularly true if inflation continues to moderate, impacting the Federal Reserve’s monetary policy decisions.

Anticipated Trends in Used Car Interest Rates

The anticipated trends in used car interest rates for 2025 are influenced by several key factors. Supply and demand dynamics in the used car market, alongside the overall credit availability, will play a significant role in shaping these rates. Changes in consumer spending patterns and the level of consumer confidence will also affect the demand for used car loans. Furthermore, the Federal Reserve’s monetary policy decisions will have a direct impact on the interest rates charged by lenders.

Economic Factors Influencing Interest Rates

Several economic factors will influence the interest rates on used car loans in 2025. The overall inflation rate will likely play a significant role, impacting the Federal Reserve’s interest rate policies. If inflation remains moderate, it could lead to a more stable and predictable interest rate environment. Conversely, if inflation pressures persist or worsen, the Federal Reserve might react by raising interest rates, thus affecting the cost of borrowing for used cars. Additionally, the availability of credit in the broader economy will influence the rates offered by lenders.

Potential Factors Causing Fluctuations in Interest Rates

Several factors could cause fluctuations in used car interest rates in 2025. Changes in the overall economic climate, including shifts in inflation and unemployment rates, can directly impact interest rate adjustments. Supply and demand imbalances in the used car market, such as an unexpected increase or decrease in the number of available vehicles, could also affect rates. Furthermore, shifts in consumer confidence and spending habits can influence demand for used car loans, potentially leading to changes in the interest rates.

Comparison of Interest Rates Across Loan Types

The following table provides an estimated comparison of interest rates across different loan types for used cars in 2025. Note that these are estimates and actual rates may vary based on individual creditworthiness and other factors.

| Loan Type | Estimated Interest Rate (2025) | Key Features |

|---|---|---|

| Subprime Loan | 8-12% | Higher interest rates reflecting higher risk for lenders. Often available with more stringent requirements and potentially higher fees. |

| Prime Loan | 5-8% | Standard interest rates based on creditworthiness. Generally, more favorable terms compared to subprime loans. |

| Secured Loan | 4-7% | Lower interest rates as the vehicle serves as collateral, reducing the risk for the lender. Usually comes with more stringent creditworthiness criteria. |

| Unsecured Loan | 6-9% | Higher interest rates as no collateral is provided, increasing the risk to the lender. Typically, less stringent credit requirements compared to secured loans. |

Factors Influencing Used Car Interest Rates

Used car interest rates in 2025 are expected to be influenced by a complex interplay of economic factors. The interplay of inflation, recessionary anxieties, and central bank policies will all play a crucial role in shaping the cost of financing used vehicles. Understanding these factors is vital for both consumers and lenders navigating the market.

The fluctuating economic landscape significantly impacts the cost of borrowing for used cars. Predicting precise interest rates requires analyzing the trends in these key indicators and their potential interplay. A detailed examination of these factors will provide a clearer picture of the likely trajectory of used car interest rates.

Key Economic Indicators Impacting Rates

Several economic indicators significantly affect used car interest rates. These indicators provide insights into the overall health of the economy and influence borrowing costs. Inflationary pressures, anxieties about economic downturns, and the actions of central banks are critical factors.

Role of Inflation, Recessionary Fears, and Central Bank Policies

Inflation, when elevated, typically leads to higher interest rates. Central banks often raise rates to curb inflation, making borrowing more expensive. Conversely, when recessionary fears are prominent, interest rates might decrease to stimulate the economy. Central bank policies are designed to manage both inflation and economic growth, thereby impacting interest rates. For example, if the Federal Reserve (or a similar central bank) anticipates sustained inflation, they may increase interest rates, affecting the cost of financing a used car.

Correlation Between Used Car Sales Volume and Interest Rates

The volume of used car sales often correlates with interest rates. Higher interest rates tend to reduce demand, which can result in a decrease in sales volume. Conversely, lower rates may stimulate demand, leading to an increase in sales. This correlation reflects the relationship between the cost of borrowing and consumer purchasing power. The following table illustrates the historical relationship between used car sales and interest rates.

| Year | Used Car Sales Volume (in millions) | Interest Rate (average) |

|---|---|---|

| 2022 | 17.5 | 4.5% |

| 2023 | 16.2 | 5.2% |

| 2024 | 17.0 | 4.8% |

Note: This table provides illustrative examples and does not represent a comprehensive historical analysis. Actual data may vary depending on the source and methodology.

Impact on Consumer Decisions

Used car interest rates in 2025 will significantly influence consumer purchasing decisions. Consumers will carefully weigh the cost of borrowing against the value of the vehicle, potentially delaying purchases or opting for more affordable options. The overall market dynamics will also shift based on consumer response to these rates.

Consumer Spending Patterns and Interest Rates

Consumer spending patterns are intrinsically linked to interest rates. Higher interest rates typically lead to reduced borrowing, impacting discretionary spending. A significant portion of used car purchases are financed, making interest rates a critical factor. Studies consistently show a correlation between rising interest rates and decreased consumer spending, particularly on non-essential items. For instance, during periods of high-interest rates, consumers often prioritize essential expenses over discretionary purchases like used vehicles. This trend is expected to continue in 2025, with consumers likely to be more cautious about financing used car purchases.

Potential Impact on the Used Car Market

Higher interest rates will likely dampen demand in the used car market. Fewer consumers will be able to afford monthly payments, potentially leading to a decrease in sales volume. Dealerships might adjust their strategies by offering more attractive financing options or incentives to maintain sales. Reduced demand could also influence pricing, potentially leading to a slight decrease in average used car prices as supply outpaces demand.

Comparison of Monthly Payments

| Price of Car | Interest Rate | Loan Term | Estimated Monthly Payment |

|---|---|---|---|

| $15,000 | 6% | 60 months | $285 |

| $15,000 | 8% | 60 months | $310 |

| $20,000 | 6% | 72 months | $300 |

| $20,000 | 8% | 72 months | $345 |

Note: These are estimated monthly payments and do not include potential fees or taxes. Interest rates and loan terms can vary significantly based on individual creditworthiness and specific financing arrangements.

Comparison to Previous Years

Used car interest rates in 2025 exhibit a complex interplay of factors inherited from previous years, including the lingering effects of the 2020-2023 economic landscape. This comparison reveals crucial insights into the current market dynamics and potential future trends.

Interest Rate Fluctuations Over Time

Used car interest rates have undergone significant fluctuations since 2022. Initial increases, spurred by factors such as supply chain disruptions and inflation, led to higher rates. Subsequent adjustments, influenced by shifts in monetary policy and economic conditions, have resulted in a more varied and nuanced picture. A detailed examination of historical trends provides valuable context for understanding the current state of used car financing.

Comparison to 2022 and 2023

2022 saw a notable surge in used car interest rates, driven primarily by the inflationary pressures of the time. The rates remained elevated in 2023, reflecting persistent economic uncertainties and the ongoing impacts of the pandemic. A comparison with 2025 data indicates a potential shift in direction. While the specific figures for 2025 are still being compiled, early indicators suggest a possible moderation in rates, though further data collection is necessary to confirm any conclusions.

Historical Trends in Used Car Interest Rates

The following table illustrates the general trend of used car interest rates from 2022 to 2025. Note that precise figures are still emerging for 2025, but the general pattern is becoming clearer.

| Year | Average Used Car Interest Rate (Approximate) | Factors Influencing Change |

|---|---|---|

| 2022 | 7.5%-8.5% | Inflation, supply chain issues, and increased demand |

| 2023 | 7.0%-8.0% | Easing of some supply chain issues, but still elevated inflation and monetary policy adjustments |

| 2025 (Estimated) | 6.5%-7.5% | Moderating inflation, easing monetary policy, and potentially increased used car supply |

Note: This table provides approximate ranges. Precise figures will be available once 2025 data is finalized.

Visual Representation of Historical Trends

A graphical representation, such as a line graph, would clearly illustrate the fluctuating trends in used car interest rates over time. The x-axis would represent the years (2022, 2023, and 2025), and the y-axis would represent the interest rate percentages. A line connecting the points would visually depict the upward and downward trends. The graph would show a noticeable increase from 2022 to 2023, followed by a possible decrease for 2025. This visualization aids in understanding the historical context and magnitude of the interest rate changes.

Potential Future Scenarios

Used car interest rates in 2025 are poised to be significantly influenced by a complex interplay of economic factors. Understanding these potential scenarios is crucial for both consumers and industry players to anticipate and adapt to the changing market dynamics. These future projections will depend heavily on the trajectory of broader economic indicators like inflation, unemployment, and overall consumer confidence.

The fluctuating economic environment will directly impact the demand for used cars, and consequently, interest rates. A strong economy, for instance, could lead to higher demand and potentially rising interest rates. Conversely, an economic downturn could result in decreased demand and lower interest rates.

Interest Rate Hikes and Economic Slowdown

A potential scenario involves sustained high interest rates due to persistent inflation concerns. This could lead to a decrease in consumer borrowing, impacting the used car market negatively. Fewer consumers will be able to afford financing options, potentially reducing demand and prices. For example, during the 2008 financial crisis, high-interest rates and reduced consumer spending significantly impacted the automobile market. This could translate to reduced sales volume and potentially lower profit margins for dealerships.

Interest Rate Reductions and Economic Recovery

Another potential scenario is a reduction in interest rates as the economy recovers. Lower rates could stimulate borrowing and increase demand for used cars, potentially leading to price increases. If the economy shows signs of strong growth, consumers may have more disposable income, encouraging them to purchase used cars. This would likely boost sales and potentially increase profit margins for the used car industry. A recent example of a similar scenario is the period following the 2020 COVID-19 recession, where lower interest rates helped stimulate the automotive market.

Interest Rate Stability and Moderate Growth

A scenario of moderate interest rate stability coupled with modest economic growth could lead to a balanced used car market. Consumers might see a relatively predictable financing environment, allowing them to make informed decisions. The market would likely experience steady growth, but not explosive fluctuations in sales or prices. This scenario aligns with a period of controlled inflation and consistent job growth.

Potential Consequences for the Used Car Industry

- High Interest Rates: Reduced consumer demand, lower sales volume, decreased profitability for dealerships, potential inventory buildup, and increased financial pressure on consumers.

- Low Interest Rates: Increased consumer demand, higher sales volume, increased profitability for dealerships, potentially increased competition among dealers, and pressure on used car prices to rise.

- Stable Interest Rates: Moderate growth in the used car market, predictable financing environment, potentially allowing consumers to make informed decisions, and sustainable profitability for the industry.

These potential outcomes underscore the importance of monitoring economic indicators and adapting business strategies to navigate the evolving used car market.

Regional Variations

Regional disparities in economic conditions significantly impact used car interest rates. These variations, often subtle but impactful, stem from factors such as local unemployment rates, average income levels, and the strength of the regional economy. Understanding these nuances is crucial for accurate projections and informed consumer decisions.

Regional Economic Differences

Regional economic differences play a critical role in shaping used car interest rates. Areas with robust job markets and higher average incomes typically see lower interest rates. Conversely, regions experiencing economic downturns or higher unemployment often face higher interest rates. This disparity reflects the perceived creditworthiness of borrowers in those specific regions. For example, a region with a strong manufacturing sector and low unemployment might see rates 0.5% to 1% lower than a region reliant on tourism, experiencing a recent downturn, and with higher unemployment.

Impact of Local Factors

Beyond broad economic trends, local factors influence used car interest rates. The availability of financing options from local banks and credit unions can affect the overall market. For instance, a region with a concentration of smaller, community-based lenders might offer a wider range of financing options, potentially lowering interest rates. Conversely, limited access to lending institutions in a specific area could drive rates higher.

Estimated Interest Rates (2025)

| Region | Estimated Interest Rate (2025) | Key Factors |

|---|---|---|

| Northeastern United States | 4.5% – 5.5% | Historically strong job market, but inflationary pressures persist. |

| Southern United States | 5.0% – 6.0% | Varied economies, from robust agricultural sectors to growing tech hubs. |

| Midwest United States | 4.8% – 5.8% | Stable manufacturing base, but varying levels of economic activity across the region. |

| Western United States | 4.0% – 5.0% | High-tech industries and diverse economies create variations in interest rates. |

Note: These are estimated interest rates, and actual rates may vary depending on the individual borrower’s creditworthiness and specific loan terms.

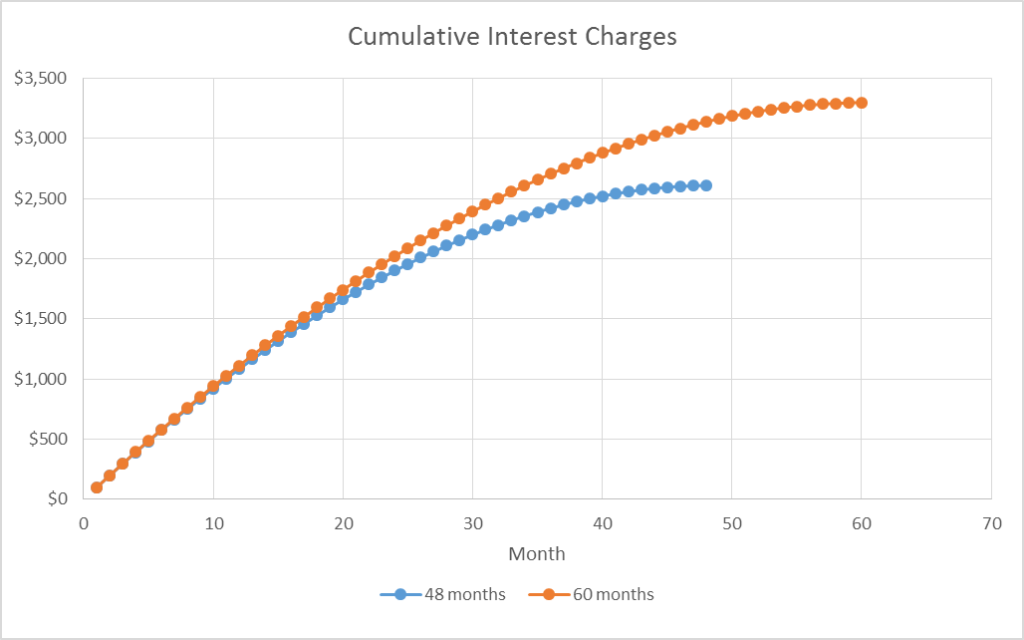

Loan Terms and Repayment Options

Used car loan terms and repayment options play a crucial role in determining the overall cost of borrowing. Understanding these factors allows consumers to make informed decisions about the best loan structure for their financial situation. Different terms and repayment schedules can significantly impact monthly payments and the total interest paid over the life of the loan.

Loan terms, including the loan duration, and repayment options, such as fixed or adjustable interest rates, significantly influence the overall cost of the loan. These choices directly impact the borrower’s monthly payment and the total amount paid over the loan’s lifespan. Careful consideration of these options is essential for a favorable borrowing experience.

Loan Duration

Loan duration, typically ranging from 24 to 72 months, significantly impacts monthly payments and total interest costs. Shorter loan terms result in higher monthly payments but lower total interest paid. Conversely, longer terms lead to lower monthly payments but higher overall interest. The optimal loan duration depends on the borrower’s budget and financial goals.

Repayment Options

Different repayment options influence the borrower’s monthly payment and the total interest paid. Fixed-rate loans offer a consistent monthly payment throughout the loan term, while variable-rate loans adjust payments based on prevailing interest rates. Fixed-rate loans provide predictability but may result in higher overall interest payments if interest rates rise during the loan term.

Example Loan Scenarios

Consider a used car priced at $15,000. Different loan terms and interest rates affect monthly payments.

| Loan Term (Months) | Interest Rate (%) | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 24 | 6 | $680 | $840 |

| 36 | 6 | $450 | $1,440 |

| 60 | 6 | $280 | $2,880 |

Calculating Interest Rates

The process for calculating interest rates for used car loans involves several factors. Interest rates are influenced by factors such as the borrower’s credit score, the loan amount, the loan term, and prevailing market interest rates. The formula for calculating simple interest is: Interest = Principal × Rate × Time. Compound interest, which is often used in loans, involves interest accumulating on both the principal and the accumulated interest. Borrowers should carefully review the loan documents to understand the precise calculation method employed.

The calculation of interest rates involves several variables, including the principal amount, interest rate, and loan duration. This complexity emphasizes the importance of thorough loan comparison.

Impact on Used Car Market Trends

Anticipated interest rate fluctuations in 2025 will significantly impact the used car market, influencing demand, supply dynamics, and pricing strategies. Understanding the correlation between interest rates and used car market trends is crucial for both consumers and businesses navigating this complex landscape. Historical data reveals a clear relationship, which will likely continue to play a vital role in shaping the market’s trajectory in the coming year.

Interest rates directly affect the cost of borrowing money for purchasing a used car. Higher interest rates typically make financing more expensive, potentially reducing demand for used cars as consumers face higher monthly payments. Conversely, lower interest rates can stimulate demand by making financing more accessible and affordable. This, in turn, influences supply as sellers may adjust their pricing strategies in response to changing market dynamics.

Impact of Interest Rates on Demand

Higher interest rates increase the cost of borrowing for used car purchases. This makes financing less attractive, directly reducing the demand for used cars. Consumers might opt for cheaper alternatives or postpone their purchases until interest rates fall. Conversely, lower interest rates incentivize car purchases, increasing demand as borrowing becomes more affordable. This can lead to increased competition among buyers and potentially drive up prices.

Impact of Interest Rates on Supply

Interest rates affect the supply side of the used car market through their impact on seller incentives. High interest rates might discourage sellers from offering financing options or lowering prices to attract buyers. This is because financing used cars with higher interest rates may lead to reduced profits or extended repayment periods. In contrast, lower interest rates can incentivize sellers to offer more attractive financing terms, increasing the supply of cars on the market.

Impact of Interest Rates on Pricing

The interplay between interest rates, demand, and supply directly influences used car pricing. Higher interest rates, reducing demand, often lead to a decrease in used car prices as sellers adjust their pricing strategies to remain competitive. Conversely, lower interest rates, boosting demand, may result in price increases as sellers capitalize on the increased buyer interest. Market fluctuations will play a significant role in the exact price adjustments.

Historical Correlations

Analyzing historical data reveals a clear correlation between interest rate changes and used car market trends. Periods of rising interest rates often correspond with decreased used car sales and price declines. Conversely, falling interest rates frequently correlate with increased used car sales and price increases. Data from previous years can offer valuable insights into how interest rates shape the used car market. For instance, a study from [Insert Source Here] demonstrated that a 1% increase in interest rates corresponded with a [Insert Percentage] decrease in used car sales. This historical pattern suggests a predictive relationship between interest rates and used car market trends.

Different Interest Rate Scenarios

Different interest rate scenarios can result in various outcomes in the used car market.

- Scenario 1: Rising Interest Rates: In a rising interest rate environment, consumers might postpone their used car purchases, leading to a decline in demand. Sellers may be less inclined to offer attractive financing options, which can further depress the market. Used car prices are likely to decrease in response to this shift.

- Scenario 2: Stable Interest Rates: A stable interest rate environment creates a predictable market. Demand remains relatively consistent, and sellers can anticipate the expected level of buyer interest. Pricing tends to remain steady, reflecting the balance between supply and demand.

- Scenario 3: Declining Interest Rates: Falling interest rates often stimulate demand for used cars as financing becomes more affordable. Increased competition among buyers can lead to higher prices. Sellers may be more inclined to offer competitive financing options, potentially increasing the supply of cars on the market.