Table of contents:

Overview of Used Car Loan Interest Rates

Used car loans are a popular financing option for purchasing a pre-owned vehicle. Understanding the interest rates associated with these loans is crucial for making informed financial decisions. Interest rates are not fixed; they vary based on a multitude of factors, impacting the total cost of the loan.

Interest rates for used car loans reflect the risk lenders take on when extending credit. The risk assessment considers various factors like the borrower’s creditworthiness and the current market conditions. Understanding these factors can help borrowers find the most favorable loan terms.

Factors Influencing Used Car Loan Interest Rates

Interest rates for used car loans are not static. Numerous factors contribute to the final interest rate a borrower receives. These factors are evaluated by lenders to determine the appropriate risk level and corresponding interest rate.

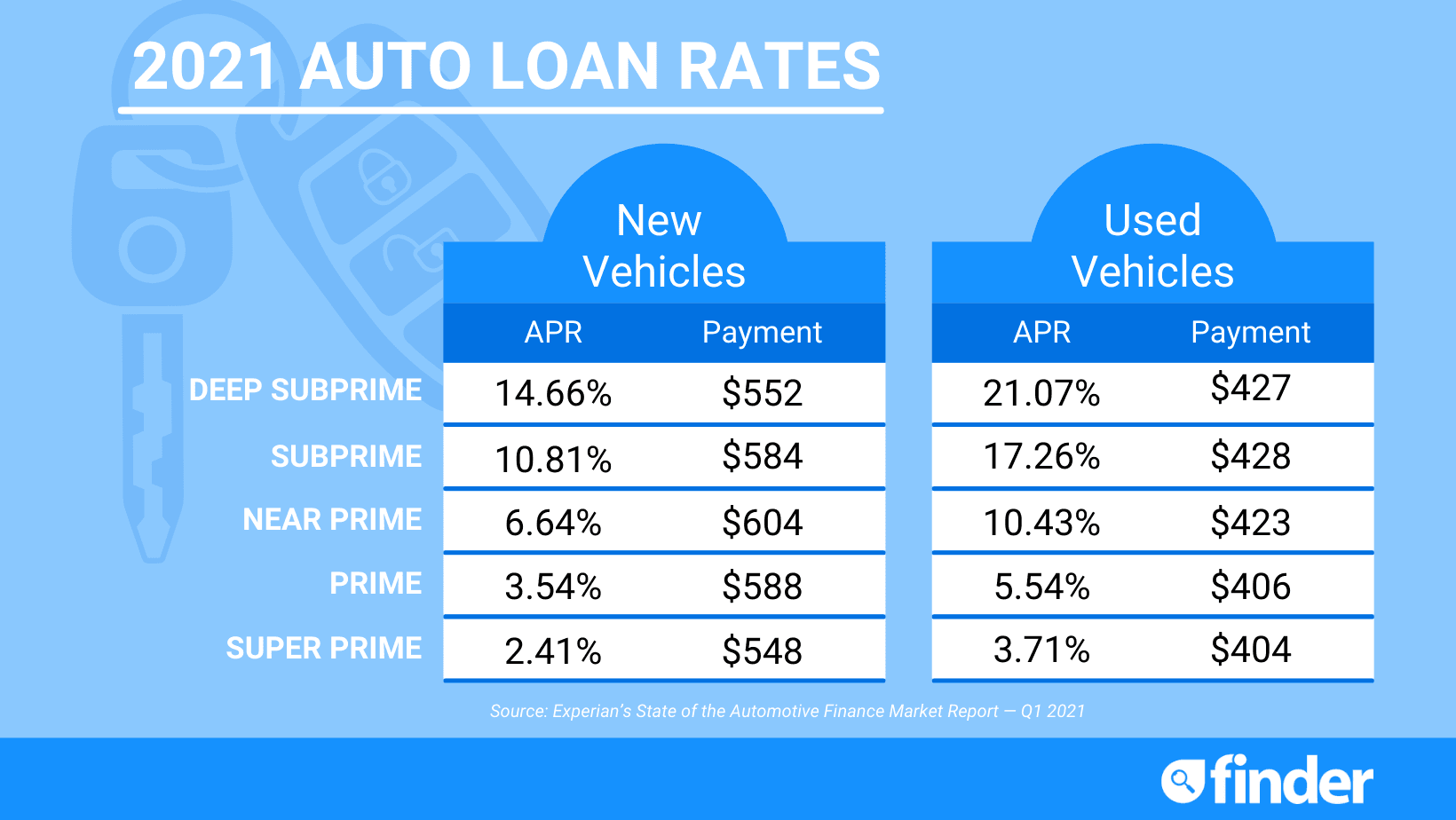

- Borrower’s Credit Score: A higher credit score typically translates to a lower interest rate. Lenders view borrowers with strong credit histories as less risky, justifying lower interest rates. For example, a borrower with a credit score above 700 is likely to receive a lower interest rate than a borrower with a credit score below 600.

- Loan Amount: Larger loan amounts often come with higher interest rates. The lender assesses the risk of the loan amount relative to the borrower’s capacity to repay it. Higher amounts may signal a greater potential risk, leading to a higher interest rate.

- Loan Term: Longer loan terms usually lead to higher interest rates. This is because the lender is extending credit over a more extended period, increasing the overall risk. For example, a 60-month loan is typically more expensive than a 24-month loan due to the longer duration.

- Current Market Conditions: Economic factors, like inflation and prevailing interest rates, can significantly impact used car loan interest rates. During periods of high inflation, interest rates tend to be higher. For instance, if the Federal Reserve raises interest rates, lenders will likely increase their rates for used car loans to reflect the higher borrowing costs.

- Vehicle Condition and Value: The overall condition and market value of the used car play a crucial role in determining the interest rate. A vehicle in excellent condition with a higher market value may command a lower interest rate compared to a vehicle with significant damage or a lower market value. This is because the vehicle’s value serves as collateral for the loan.

- Type of Lender: Different lenders have varying lending policies and risk assessments. Banks, credit unions, and online lenders may have different interest rates for used car loans. A comparison across lenders is essential for obtaining the best possible interest rate.

Comparison of Interest Rates Across Different Lenders

Comparing interest rates across various lenders is vital for securing the most favorable loan terms. Different lenders may have varying criteria for evaluating loan applications and offer different rates for similar borrowers. This comparison can help borrowers find the best deals.

- Banks: Often have competitive rates, but the application process may be more complex. Banks may be more cautious and stringent with lending practices.

- Credit Unions: May offer lower rates to members. The rates depend on the credit union’s policies.

- Online Lenders: Frequently provide streamlined online application processes and competitive rates. Online lenders may have a broader range of interest rates available, often adjusting to current market trends.

Typical Interest Rates Based on Credit Scores

Borrowers with different credit scores may experience varying interest rates. This table provides an illustrative overview of typical interest rates for used car loans across different credit scores. Keep in mind that these are just averages, and actual rates may vary.

| Credit Score Range | Typical Interest Rate |

|---|---|

| Low (500-600) | 15-20% |

| Medium (601-700) | 10-15% |

| High (701-850) | 5-10% |

Loan Terms and Corresponding Interest Rates

The loan term significantly impacts the total cost of the loan. A longer loan term means more interest paid over the life of the loan.

| Loan Term (Months) | Typical Interest Rate |

|---|---|

| 24 | 7-12% |

| 36 | 8-13% |

| 60 | 9-14% |

Factors Affecting Interest Rates

Used car loan interest rates are influenced by a complex interplay of factors. Understanding these elements is crucial for borrowers to make informed decisions and secure the most favorable loan terms. This section delves into the key determinants of used car loan interest rates.

Credit Score

A borrower’s credit score is a significant factor in determining the interest rate for a used car loan. Lenders use credit scores to assess the borrower’s creditworthiness and risk. Higher credit scores typically translate to lower interest rates, as they indicate a lower likelihood of default. This is because borrowers with strong credit histories demonstrate a responsible approach to financial obligations.

Loan Amount and Loan Term

The amount borrowed and the duration of the loan (loan term) also affect the interest rate. Generally, larger loan amounts and longer loan terms come with higher interest rates. This is because the lender assumes a greater financial risk with a larger amount and longer repayment period. The lender’s risk increases with the loan amount and term due to the extended period over which the principal must be repaid. For example, a loan for $15,000 over 72 months carries a higher risk than a loan for $5,000 over 36 months.

Current Market Interest Rates

The prevailing market interest rates play a significant role in shaping used car loan interest rates. When overall market interest rates increase, used car loan interest rates tend to rise as well. This is a direct correlation; higher market rates translate to higher borrowing costs for all types of loans, including used car loans. For example, if the Federal Reserve raises its benchmark interest rate, lenders are likely to increase their rates to maintain profitability.

Lender’s Risk Assessment

Lenders evaluate various factors to assess the risk associated with a loan application. These factors include the borrower’s credit history, income stability, and debt-to-income ratio. A higher perceived risk often results in a higher interest rate. Lenders use this risk assessment to determine the potential for default and adjust the interest rate accordingly. A lender’s risk assessment includes a comprehensive review of the applicant’s financial profile.

Loan Programs

Government-backed loan programs, such as those offered by the Small Business Administration (SBA), often have lower interest rates compared to conventional loans. These programs offer favorable terms due to the reduced risk perceived by the lender. This is because the government acts as a guarantor for a portion of the loan, reducing the lender’s financial exposure.

Down Payments

A larger down payment typically leads to a lower interest rate. A larger down payment reduces the loan amount, which in turn lowers the lender’s risk. This is because a larger down payment reduces the outstanding balance, decreasing the amount at risk if the borrower defaults. For instance, a $2,000 down payment on a $10,000 car loan will result in a lower interest rate than a loan with no down payment.

Credit Score and Interest Rate Relationship

| Credit Score Range | Estimated Interest Rate (Example) |

|---|---|

| 700-759 | 4.5%-6.0% |

| 760-850 | 3.0%-5.5% |

This table illustrates a potential relationship between credit scores and interest rates for used car loans. Note that these are example rates and actual rates may vary based on other factors. The table showcases how higher credit scores correlate with lower interest rates.

Loan Programs and Options

Securing financing for a used car involves navigating various loan programs. Understanding the available options, their associated terms, and the pros and cons of each is crucial for making an informed decision. Choosing the right loan program can significantly impact your monthly payments and overall cost of the vehicle.

Different lenders offer tailored programs with varying interest rates, fees, and application processes. This section details the common loan programs, their key characteristics, and how they compare to one another, helping you select the best fit for your financial situation and needs.

Dealer Financing

Dealer financing is a common option offered directly by the dealership. This often involves working with the dealership’s in-house lender, which can streamline the process.

- Advantages: Ease of access, potentially quicker approval times, and familiarity with the dealership. Some dealerships may offer special incentives or bundled packages that include financing.

- Disadvantages: Interest rates may be higher compared to other options, and the selection of loan terms might be limited. Dealers may have less competitive rates, and you may be pressured to accept the financing they offer.

Bank Financing

Banks offer a range of used car loan programs. They typically have established lending criteria and may provide more competitive interest rates than dealer financing, depending on your creditworthiness.

- Advantages: Potentially lower interest rates than dealer financing, broader range of loan terms, and the opportunity to negotiate loan terms.

- Disadvantages: The application process might take longer, requiring more documentation and possibly a credit check. You may need to meet specific lending criteria, such as a certain credit score.

Online Lenders

Online lenders have become increasingly popular for used car financing. They offer convenient online application processes and potentially competitive interest rates.

- Advantages: Faster application process compared to traditional lenders, access to a broader range of loan options, and potentially lower interest rates, especially for borrowers with strong credit.

- Disadvantages: Lenders may have specific criteria for approval. You might not have the same level of direct contact with a loan officer, which could limit your ability to ask questions and clarify issues.

First-Time Buyer Programs

Some lenders offer specialized programs for first-time car buyers. These programs often come with flexible lending criteria and potentially lower interest rates to encourage car ownership for this demographic.

- Example: A credit union might offer a lower interest rate for first-time car buyers who are new members and demonstrate a strong financial commitment.

Loan Program Comparison

The following table provides a comparison of loan programs based on interest rates, fees, and application processes.

| Loan Program | Interest Rate | Fees | Application Process |

|---|---|---|---|

| Dealer Financing | Moderate to High | Potentially higher documentation fees | Generally quicker |

| Bank Financing | Moderate to Low (depending on creditworthiness) | Possible closing costs and origination fees | May be more time-consuming |

| Online Lenders | Moderate to Low (depending on creditworthiness) | Potential origination fees, or no fees | Generally quick and online |

Shopping for the Best Rates

Securing the most favorable interest rate for your used car loan is crucial for minimizing the overall cost of financing. Understanding the strategies for finding competitive rates and the steps to compare offers from different lenders empowers you to make an informed decision. This process involves meticulous research, proactive communication, and a strategic approach to negotiation.

Finding the best used car loan interest rate is a multifaceted process requiring careful planning and execution. It involves researching lenders, comparing offers, and potentially negotiating terms. Pre-approval can significantly enhance your bargaining position, and online tools offer efficient ways to compare rates from multiple lenders.

Strategies for Finding Competitive Rates

Thorough research is essential for identifying the most competitive interest rates. This includes exploring various lenders, understanding their loan programs, and evaluating their terms and conditions. Comparing rates from different lenders is a critical step in securing the best possible financing. Utilizing online comparison tools and contacting multiple lenders directly are both effective strategies.

Steps to Compare Interest Rates

A structured approach to comparing interest rates is essential for maximizing your chances of securing a favorable loan. The process begins by identifying potential lenders, gathering information on their interest rates and loan programs, and comparing the terms and conditions. This involves contacting lenders directly, using online comparison tools, and evaluating factors like loan terms, fees, and repayment options.

- Identify Potential Lenders: Research and compile a list of lenders offering used car loans. Consider online lenders, banks, credit unions, and dealerships.

- Gather Information: Request loan terms, interest rates, and any associated fees from each lender. Obtain detailed information on loan amounts, repayment periods, and prepayment penalties.

- Compare Loan Terms: Evaluate the loan programs offered by each lender, focusing on interest rates, fees, and loan terms. Consider factors such as the loan amount, repayment period, and any additional charges.

- Evaluate Lender Reputation: Research the reputation of each lender to assess their reliability and commitment to customer satisfaction. Review online reviews and consider the lender’s financial stability.

Shopping for Used Car Loans Online

Online resources offer convenient and efficient ways to compare used car loan interest rates from multiple lenders. Using online comparison tools can streamline the process of gathering information and identifying the best rates. Online platforms often allow you to input your desired loan amount, credit score, and other relevant details to receive tailored interest rate quotes. This significantly reduces the time and effort required to compare offers.

- Utilize Online Comparison Tools: Leverage online platforms that aggregate loan offers from multiple lenders. These tools simplify the comparison process and allow you to quickly identify the best rates.

- Browse Lender Websites: Directly visit the websites of lenders offering used car loans to explore their loan programs and associated interest rates. Compare terms, conditions, and fees to determine the most suitable option.

- Seek Quotes from Multiple Lenders: Submit loan requests to multiple lenders online to obtain personalized interest rate quotes. Compare the quotes received to identify the most competitive rates.

The Importance of Pre-Approval

Obtaining pre-approval for a used car loan significantly strengthens your position when negotiating with lenders. Pre-approval provides a clear understanding of the loan amount and interest rate you qualify for, allowing you to confidently negotiate with dealerships and lenders. This gives you a baseline for comparison and empowers you to make informed decisions.

- Understanding Your Financing Options: Pre-approval allows you to know your financing limitations, helping you avoid overspending or accepting less favorable terms.

- Negotiating Power: Armed with a pre-approval letter, you’ll have more leverage when negotiating with sellers and lenders. This knowledge strengthens your position and helps you secure the best possible interest rate.

- Avoid Last-Minute Surprises: Pre-approval eliminates the uncertainty of loan approval during the purchase process, ensuring a smoother transaction.

Negotiating Interest Rates

Negotiating interest rates effectively requires a strategic approach and a clear understanding of your financial situation. While aggressive negotiation isn’t always effective, presenting a well-reasoned argument and highlighting your financial strength can sometimes lead to favorable interest rate adjustments. This often involves demonstrating a strong credit history and financial stability.

- Know Your Credit Score: Understanding your credit score is crucial for assessing your negotiating power. A higher credit score often translates to better interest rates.

- Research Market Rates: Thoroughly research current market interest rates for used car loans. This knowledge provides a strong foundation for negotiating favorable terms.

- Present a Compelling Argument: Clearly articulate your financial situation and demonstrate your commitment to repaying the loan. Highlight any favorable financial factors, such as a strong credit history or consistent income.

Securing the Best Possible Interest Rate

A step-by-step approach to securing the best possible interest rate for a used car loan involves careful planning and execution. This includes researching lenders, comparing rates, obtaining pre-approval, and strategically negotiating terms. This structured process increases the likelihood of obtaining favorable financing.

- Research Lenders: Identify potential lenders offering used car loans and gather information on their loan programs.

- Compare Rates: Use online tools and contact multiple lenders to compare interest rates and associated fees.

- Obtain Pre-Approval: Secure pre-approval from a lender to establish your financing capacity and negotiate effectively.

- Negotiate Terms: Present a well-reasoned argument, highlighting your financial strength and research on market rates.

- Finalize the Loan: Review all loan documents thoroughly and ensure they accurately reflect the agreed-upon terms before signing.

Understanding Loan Terms and Conditions

Navigating the intricacies of a used car loan requires a keen understanding of the terms and conditions. These stipulations dictate the borrower’s obligations and the lender’s rights, impacting everything from monthly payments to potential penalties. Thorough review is crucial to avoid unexpected financial burdens down the line.

Significance of Loan Terms and Conditions

Understanding the fine print of a used car loan is paramount. It protects borrowers from hidden fees and ensures they are aware of their financial responsibilities. Clear comprehension of the terms allows for informed decision-making and prevents potential surprises during the loan’s lifespan.

Meaning of Different Loan Terms

Loan documents often use specialized terminology. Understanding these terms is essential for effective negotiation and responsible borrowing.

- Annual Percentage Rate (APR): The APR reflects the total cost of borrowing, including interest and fees, expressed as a yearly percentage. A lower APR generally translates to lower monthly payments. For example, a 5% APR on a $10,000 loan could lead to significantly different monthly payments compared to a 7% APR.

- Loan Term: This represents the duration of the loan, typically expressed in months or years. A longer term often means lower monthly payments but results in more interest paid over the loan’s life. For example, a 36-month loan will have more frequent payments than a 60-month loan.

- Fees: Various fees can be associated with a used car loan, including origination fees, processing fees, and late payment penalties. These fees can significantly impact the overall cost of borrowing. For example, a $500 origination fee on a $15,000 loan can have a noticeable effect on the total cost of the loan.

Importance of Prepayment Penalties and Other Clauses

Prepayment penalties and other clauses can affect borrowers’ ability to repay the loan early. It’s crucial to understand these provisions before committing to a loan.

- Prepayment Penalties: Some lenders impose penalties if the loan is paid off before the agreed-upon term. Understanding these penalties is critical for financial planning. A prepayment penalty of 2% of the remaining loan balance for early repayment could represent a substantial financial burden if the borrower decides to pay off the loan early.

- Late Payment Penalties: These penalties are charged if monthly payments are not made on time. Knowing the late payment penalty amount can help borrowers manage their finances effectively. A late payment penalty of $25 or more could quickly add up over time if not paid promptly.

- Default Clause: This clause Artikels the consequences of failing to meet the terms of the loan agreement, including potential repossession of the vehicle. Comprehending these consequences is vital to responsible borrowing.

Examples of Common Loan Terms and Conditions

Different lenders will have varying terms and conditions. Reviewing examples can provide a better understanding.

A typical used car loan might include a 6% APR, a 60-month loan term, a $100 origination fee, and a 2% prepayment penalty if the loan is paid off within the first 24 months.

Another loan agreement could feature a 7% APR, a 48-month term, no origination fee, and no prepayment penalty.

Loan Terms and Conditions Comparison

A table illustrating differences in loan terms across various lenders is presented below.

| Lender | APR (%) | Loan Term (Months) | Origination Fee ($) | Prepayment Penalty (%) |

|---|---|---|---|---|

| Lender A | 6.5 | 60 | 150 | 2 |

| Lender B | 7.0 | 48 | 0 | 0 |

| Lender C | 6.0 | 72 | 100 | 1 |

Impact of Economic Conditions

Used car loan interest rates are intrinsically linked to the broader economic climate. Fluctuations in inflation, recessionary pressures, and shifts in Federal Reserve monetary policy all directly influence the cost of borrowing for used car purchases. Understanding these dynamics is crucial for consumers seeking the most favorable loan terms.

Influence of Inflation

Inflation, characterized by a general increase in prices, typically leads to higher interest rates. Lenders adjust rates to compensate for the diminishing purchasing power of money. As prices rise, the real value of the loan repayments decreases, necessitating higher interest rates to maintain profitability. This inflationary pressure often translates into higher borrowing costs for consumers across various sectors, including used car loans. For instance, during periods of high inflation, lenders might increase interest rates to safeguard against the erosion of the loan’s real value.

Effect of Recession

Recessions, marked by economic downturns, often result in lower interest rates, but this is not always the case. During a recession, the Federal Reserve might reduce interest rates to stimulate economic activity. Lower interest rates encourage borrowing and spending, boosting economic growth. However, the impact on used car loan interest rates depends on various factors, including the severity of the recession and the overall financial health of the borrower. In some cases, a recessionary period might lead to reduced demand for loans, impacting interest rates, while in others, lenders might increase rates to manage risk in a challenging economy.

Impact of Federal Reserve Monetary Policy

The Federal Reserve (the Fed) plays a pivotal role in setting the direction of interest rates. The Fed’s monetary policy decisions, including adjustments to the federal funds rate, directly influence borrowing costs. When the Fed raises interest rates, borrowing becomes more expensive, impacting used car loan rates. Conversely, when the Fed lowers rates, borrowing becomes cheaper, potentially influencing used car loan interest rates. The Fed’s policy actions are designed to maintain price stability and maximum employment, and these actions directly influence the cost of credit for consumers and businesses alike. For example, during periods of high inflation, the Fed might raise rates to curb spending and slow the pace of price increases, leading to higher used car loan interest rates.

Examples of Past Economic Events

Past economic events have provided clear examples of how economic conditions influence used car loan interest rates. The 2008 financial crisis, for instance, saw interest rates fall significantly as the Fed implemented measures to stimulate the economy. In contrast, periods of high inflation, such as the 1970s, were associated with substantially higher interest rates for various loans, including those for used cars. These historical trends highlight the interconnectedness between economic conditions and borrowing costs.

Table: Economic Indicators and Interest Rates

| Economic Indicator | Impact on Interest Rates | Example |

|---|---|---|

| Inflation | Higher inflation typically leads to higher interest rates. | High inflation in the 1970s resulted in significantly higher interest rates for various loans. |

| Recession | Recessions can lead to lower interest rates as the Fed stimulates the economy. | The 2008 financial crisis saw a decrease in interest rates to stimulate economic activity. |

| Federal Reserve Policy | The Fed’s decisions on interest rates directly impact used car loan rates. | When the Fed raises the federal funds rate, borrowing costs increase. |

Tips for Managing Used Car Loan Payments

Successfully managing your used car loan payments is crucial for maintaining a positive credit history and avoiding financial strain. This involves proactive strategies to ensure timely payments and potentially reduce the overall loan duration. Understanding the importance of consistent payments and the implications of defaulting is key to responsible car ownership.

Strategies for Avoiding Late Payments

Consistent budgeting and planning are essential to avoid late payments. Develop a realistic budget that incorporates the car loan payment into your monthly expenses. Track your income and expenses meticulously to ensure the loan payment fits within your financial capacity. Set up automatic payments from your bank account to the lender. This eliminates the risk of forgetting to make a payment. Review your monthly bank statements to confirm that payments are processed correctly. Consider contacting the lender immediately if you anticipate difficulty in making a payment. Most lenders are willing to work with borrowers who demonstrate financial hardship and communicate their situation proactively. Early communication can prevent a late payment and potentially negative consequences.

Methods for Making Extra Payments

Making extra payments can significantly reduce your loan term and total interest paid. Consult your loan agreement to understand the implications of making extra payments. Some loans allow for lump-sum payments, while others might only accept them on a monthly basis. Create a savings plan to allocate extra funds specifically for car loan repayment. If possible, allocate a portion of your monthly income to the loan’s principal amount. This can significantly shorten the repayment period. Consider setting up a high-yield savings account to ensure consistent interest on your extra funds.

Consequences of Defaulting on a Used Car Loan

Defaulting on a used car loan has serious repercussions. Lenders can take legal action, leading to repossession of the vehicle, damage to your credit score, and potential lawsuits for the outstanding balance. The negative impact on your credit score can significantly affect your ability to secure loans or credit in the future, impacting your access to various financial services and opportunities. Repossession can result in significant financial losses and difficulties in obtaining another vehicle loan.

Payment Strategies and Potential Benefits

| Payment Strategy | Potential Benefits |

|---|---|

| Consistent, on-time payments | Maintains positive credit history, avoids late fees, and prevents repossession. |

| Extra Principal Payments | Shortens the loan term, reduces the total interest paid, and frees up funds for other financial goals. For example, a $500 extra payment per month on a $20,000 loan at 6% interest can shorten the loan term by approximately 12 months. |

| Automatic Payments | Eliminates the risk of forgetting payments, ensures consistent loan repayments, and promotes better financial discipline. |

| Budgeting and Financial Planning | Ensures the car loan payment fits within your financial capacity, prevents late payments, and enables proactive management of finances. |

| Communicating with Lender | Demonstrates responsible borrowing and provides opportunities to address potential financial hardship, avoiding default and negative credit implications. |