Overview of Used Car Finance Rates

Used car finance rates represent the interest charged on loans for purchasing a used vehicle. These rates are crucial for both buyers and sellers, as they directly impact the cost of borrowing and the profitability of a sale. Understanding these rates allows consumers to make informed financial decisions and businesses to structure competitive financing options.

Used car finance rates are influenced by a complex interplay of factors. These rates are not static; they fluctuate based on a multitude of economic conditions, market trends, and lender-specific policies. Several variables contribute to the final interest rate a borrower receives.

Factors Influencing Used Car Finance Rates

Various factors play a significant role in determining the interest rates for used car loans. Lenders meticulously assess these factors to calculate the risk associated with each loan application. The most influential factors include the borrower’s creditworthiness, the vehicle’s condition and value, and the prevailing economic climate. These factors, when considered collectively, paint a clear picture of the borrower’s ability to repay the loan.

Typical Range of Rates for Different Credit Profiles

Used car finance rates vary considerably depending on the borrower’s credit history. A strong credit score generally translates to lower interest rates, as it indicates a lower risk of default. Conversely, borrowers with lower credit scores will typically face higher interest rates.

- Excellent credit (e.g., FICO score above 740): Borrowers with excellent credit often qualify for rates below 5% for a used car loan.

- Good credit (e.g., FICO score between 680 and 739): These borrowers might see rates ranging from 5% to 8%.

- Fair credit (e.g., FICO score between 620 and 679): Borrowers in this category may experience rates from 8% to 12% or higher.

- Poor credit (e.g., FICO score below 620): Individuals with poor credit often face significantly higher rates, sometimes exceeding 15% or more.

Comparison of Rates Across Loan Terms

The loan term, or the duration over which the loan is repaid, also impacts the interest rate. Generally, longer loan terms result in lower monthly payments but potentially higher total interest paid over the loan’s life.

| Loan Term (months) | Estimated Rate Range (Example) |

|---|---|

| 24 | 6% – 10% |

| 36 | 5% – 9% |

| 48 | 4.5% – 8.5% |

| 60 | 4% – 8% |

Note: These are illustrative examples and actual rates will vary based on individual circumstances.

Different Types of Used Car Financing

Securing financing for a used car involves exploring various options, each with unique advantages and disadvantages. Understanding these choices empowers you to make informed decisions that align with your financial situation and borrowing needs. Different lenders employ distinct approval processes and interest rates, impacting the overall cost of your purchase.

Choosing the right financing method can significantly influence your monthly payments and the total cost of ownership for the vehicle. A comprehensive understanding of the available options allows you to compare terms, rates, and fees, ensuring a financially sound and beneficial transaction.

Common Used Car Financing Options

Various financial institutions and intermediaries offer used car financing options. Understanding the common types helps you evaluate the most suitable choice.

- Bank Loans: Banks often offer competitive interest rates, particularly for borrowers with established credit histories and strong financial profiles. The approval process typically involves comprehensive credit checks and documentation verification. A significant advantage is the potential for longer repayment terms, allowing for more manageable monthly payments. However, the application process can be more rigorous than some other options. For instance, a borrower with a strong credit score and a stable employment history might secure a loan with a lower interest rate and longer repayment period from a bank compared to a dealer financing option.

- Dealer Financing: Many dealerships partner with lending institutions to offer in-house financing. This can streamline the process, often eliminating the need for extensive paperwork and multiple applications. However, interest rates might not always be as competitive as those offered by independent lenders. The approval process is often more straightforward and faster, potentially helping the buyer complete the purchase more quickly. For example, a buyer with a good credit history and a down payment may receive a favorable rate from a dealer compared to an online lender. However, this may not always be the case.

- Online Lenders: Online lenders have become increasingly popular for used car financing, offering a more streamlined and often faster application process. These lenders often utilize online platforms to collect and process information, which can be more convenient. Interest rates can vary widely based on creditworthiness and other factors. The approval process often involves an online application and credit check, making it relatively quick. For example, a borrower with a high credit score and a solid financial history could qualify for a lower interest rate from an online lender compared to a dealer loan, although this is not always the case.

Comparison of Approval Processes

The approval process for used car financing varies significantly depending on the lender. Understanding these differences is critical for a smooth transaction.

- Bank Loans: Banks typically require thorough credit checks, income verification, and detailed documentation. This rigorous process ensures the lender assesses the borrower’s financial stability and ability to repay the loan.

- Dealer Financing: Dealer financing often involves a more streamlined process, with less paperwork and faster approvals. However, the credit standards may differ from those used by independent lenders.

- Online Lenders: Online lenders typically employ a simplified online application process. Credit checks are conducted rapidly, and the application can be completed within a short timeframe. The lender considers the borrower’s credit history and other financial data to determine the interest rate and approval.

Typical Interest Rates

Interest rates charged by lenders vary widely. Factors such as credit score, loan amount, and the term of the loan influence the rate.

| Lender Type | Typical Interest Rate Range (Example) |

|---|---|

| Bank Loans | 4-10% |

| Dealer Financing | 5-12% |

| Online Lenders | 6-14% |

Note: These are example ranges and actual rates can vary significantly.

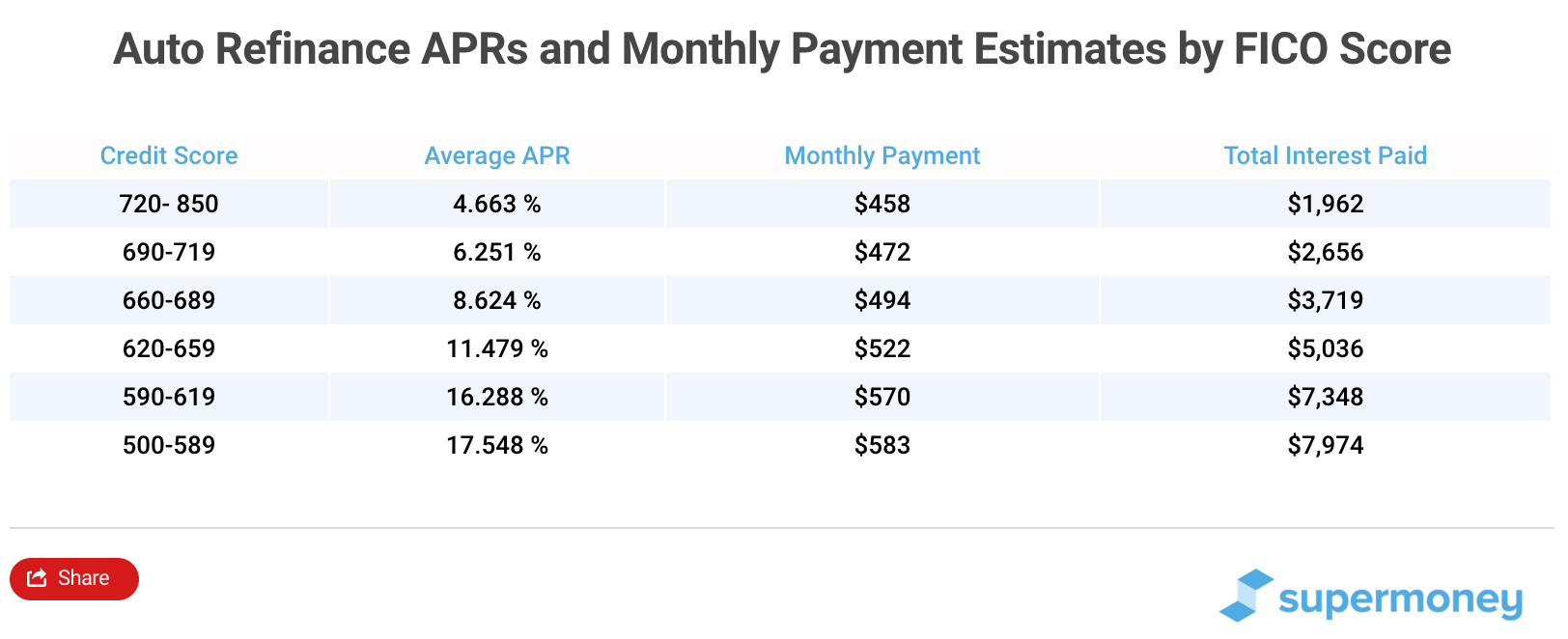

Impact of Credit Score on Used Car Finance Rates

Your credit score significantly influences the interest rate you’ll be offered for a used car loan. Lenders use credit scores to assess your creditworthiness, determining the risk of lending you money. A higher score indicates a lower risk, leading to more favorable financing terms.

Understanding the direct correlation between credit score and financing rates is crucial for securing the best possible deal. Different credit scores result in varied interest rates, impacting the overall cost of the loan. A strong credit history, reflected in a high credit score, unlocks lower interest rates and increased loan approval chances. Conversely, a lower credit score typically means higher interest rates and a reduced likelihood of loan approval.

Credit Score and Interest Rate Impact

Lenders meticulously analyze credit scores to determine the risk associated with granting a loan. A higher credit score typically translates to a lower interest rate, as lenders perceive less risk in lending to borrowers with a proven track record of responsible financial management. Conversely, lower credit scores signify a higher risk, leading to higher interest rates.

Impact on Loan Approval Likelihood

Credit history directly impacts the likelihood of loan approval. A strong credit history, demonstrated by a high credit score, significantly increases the chances of loan approval. Conversely, a poor credit history, indicated by a low credit score, decreases the probability of loan approval. This is because lenders are more likely to approve loans for borrowers with a history of timely payments and responsible financial behavior.

Potential Rate Difference by Credit Score

The following table illustrates the potential difference in interest rates for a used car loan of $10,000, based on varying credit scores. These figures are illustrative and may vary based on the specific lender, the car’s condition, and other loan terms.

| Credit Score Range | Estimated Interest Rate |

|---|---|

| 700-850 (Excellent) | 4.5% – 6.5% |

| 650-699 (Good) | 6.5% – 8.5% |

| 600-649 (Fair) | 8.5% – 11.5% |

| Below 600 (Poor) | 11.5% – 15% + |

Factors Affecting Loan Terms

Securing financing for a used car involves navigating various factors that directly influence the loan terms offered. Understanding these elements is crucial for securing the most favorable financing options. Loan terms, including interest rates and repayment durations, are not static and vary based on a multitude of factors.

The vehicle’s condition, down payment amount, and trade-in value are significant determinants of the loan terms. Each factor interacts with others, shaping the final financing package. A comprehensive understanding of these relationships empowers buyers to make informed decisions and secure the most suitable loan terms.

Vehicle Condition and Loan Term

The overall condition of the used vehicle significantly impacts the loan term. A well-maintained vehicle with minimal wear and tear is perceived as a lower risk by lenders. This translates to a potentially lower interest rate and a longer loan term. Conversely, a vehicle with significant mechanical issues or extensive damage is deemed higher risk. Lenders may impose a shorter loan term and a higher interest rate to mitigate their risk exposure. This approach ensures that the lender is not exposed to potential future repair costs that could impact the loan’s profitability.

Down Payment and Loan Term

The down payment amount directly influences both the loan term and the interest rate. A larger down payment reduces the loan amount, decreasing the lender’s risk. This often leads to a lower interest rate and potentially a shorter loan term. Conversely, a smaller down payment results in a larger loan amount, increasing the lender’s risk. This may lead to a higher interest rate and a longer loan term. A higher down payment allows the buyer to take advantage of potentially better terms, which ultimately saves money in the long run.

Trade-in Value and Loan Amount

A trade-in vehicle’s value plays a critical role in determining the loan amount. A higher trade-in value can reduce the loan amount needed to purchase the new used car. This reduction in loan amount diminishes the lender’s risk, potentially leading to a lower interest rate and a shorter loan term. Conversely, a lower trade-in value will necessitate a larger loan amount, increasing the lender’s risk and potentially resulting in a higher interest rate and a longer loan term.

Scenarios Illustrating Loan Terms and Rates

The table below illustrates various scenarios and their associated loan terms and rates. These examples highlight the interaction between vehicle condition, down payment, and trade-in value in shaping the final loan package.

| Scenario | Vehicle Condition | Down Payment ($) | Trade-in Value ($) | Loan Amount ($) | Interest Rate (%) | Loan Term (months) |

|---|---|---|---|---|---|---|

| 1 | Excellent | 5,000 | 2,000 | 15,000 | 4.5 | 60 |

| 2 | Good | 2,000 | 1,000 | 18,000 | 5.5 | 72 |

| 3 | Fair | 1,000 | 500 | 20,000 | 6.5 | 84 |

These are simplified examples, and actual rates and terms will vary based on individual creditworthiness, lender policies, and market conditions.

Comparison of Financing Options for Different Car Types

Used car financing rates aren’t uniform across all vehicle types. Factors like vehicle size, age, and condition significantly influence the interest rates and terms offered by lenders. Understanding these nuances can help potential buyers secure the most favorable financing options.

Impact of Vehicle Type on Financing Rates

Different car types often come with varying financing rates. This disparity stems from several key factors. For instance, larger and heavier vehicles, such as SUVs and trucks, may have slightly higher financing rates than smaller, more economical sedans. This difference is often due to the increased risk lenders perceive with these larger vehicles. Also, the potential for increased maintenance costs and repair expenses might contribute to the difference in interest rates. Sedans, with their typically lower maintenance needs, can command more favorable rates.

Influence of Vehicle Age and Mileage

The age and mileage of a used car are critical determinants in financing terms. Generally, older vehicles with higher mileage will have higher interest rates. Lenders consider the vehicle’s depreciation rate and potential for costly repairs when assessing the risk associated with financing older models. This is because older vehicles are more likely to require costly maintenance or repair work, increasing the risk for the lender. Moreover, the decreased resale value of older vehicles further contributes to the higher financing rates. Conversely, newer, lower-mileage vehicles typically attract more favorable financing rates due to their lower risk profile.

Impact of Make and Model on Financing Terms

The specific make and model of a used car also play a role in determining financing terms. Certain brands and models have a reputation for reliability and lower maintenance costs. These factors often translate into more favorable interest rates and longer loan terms. Similarly, vehicles with established warranties or service history from reputable dealerships can lead to more attractive financing options. On the other hand, models known for high maintenance or repair costs may result in higher rates and shorter loan terms.

Average Interest Rates by Car Type

| Car Type | Average Interest Rate (Estimated) |

|---|---|

| Sedans | 5.5%-7.5% |

| SUVs | 6.0%-8.0% |

| Trucks | 6.5%-8.5% |

Note: These are estimated average interest rates and may vary based on individual creditworthiness, loan amount, and other factors. These figures should be used as a general guide only and are not a guarantee of the actual rates offered.

Tips for Obtaining the Best Used Car Finance Rates

Securing the most favorable used car finance rates hinges on a combination of proactive preparation and strategic negotiation. Understanding the factors influencing these rates, and actively employing proven techniques, empowers you to secure the best possible terms for your purchase. This involves more than just comparing interest rates; it encompasses a holistic approach to the entire financing process.

Effective strategies for obtaining lower rates encompass meticulous preparation, informed decision-making, and proactive communication with lenders. A comprehensive understanding of the process allows for the identification of potential pitfalls and the implementation of mitigating strategies, ultimately leading to more favorable financing terms.

Strategies for Lower Rates

Lowering your used car finance rates necessitates a multifaceted approach, focusing on factors such as creditworthiness, loan terms, and lender comparisons. A well-prepared loan application, demonstrating financial stability, significantly influences the interest rate offered.

- Improve Your Credit Score: A higher credit score translates directly to lower interest rates. Paying all bills on time, managing existing debts responsibly, and avoiding new credit applications in the near term can positively impact your credit rating. For example, a 5-point improvement in your credit score could translate to a 0.5% reduction in your interest rate.

- Negotiate Loan Terms: While interest rates are crucial, the loan term length also affects the overall cost. A longer loan term may result in lower monthly payments but could increase the total interest paid over the life of the loan. Consider the trade-offs between lower monthly payments and overall cost.

- Compare Multiple Lenders: Don’t limit yourself to a single lender. Thoroughly compare interest rates, fees, and terms from various banks, credit unions, and online lenders. This comparative analysis empowers you to select the most advantageous financing option.

Importance of Comparing Offers

Comparing financing offers from different lenders is critical for obtaining the most competitive used car finance rates. This process requires careful evaluation of not only interest rates but also associated fees and terms.

- Identify Key Differences: Scrutinize the specific terms of each offer, paying close attention to interest rates, loan fees, and any additional charges. Note the difference in origination fees and prepayment penalties, if any. A comprehensive comparison spreadsheet can be invaluable in this process.

- Understand Loan Terms: Pay attention to the loan’s terms, such as the loan amount, interest rate, and loan duration. This will help in identifying potential discrepancies and negotiating the best possible rates. For example, a 60-month loan might have a lower monthly payment but a higher total interest cost compared to a 48-month loan.

- Consider Hidden Costs: Be wary of any hidden fees or charges that might be associated with the loan. Carefully read the fine print of each offer to ensure that you understand all the costs involved.

Preparing a Strong Loan Application

A well-prepared loan application significantly influences the likelihood of receiving favorable financing terms. This involves accurate and complete information, demonstrating responsible financial management.

- Accurate Information: Provide accurate and complete information on your income, debts, and credit history. Inaccuracies can negatively impact your application and increase the chances of loan denial.

- Strong Credit History: A positive credit history, demonstrating consistent repayment of debts, significantly enhances your application. This includes paying bills on time, avoiding late payments, and maintaining a low debt-to-income ratio.

- Documentation: Ensure you have all necessary documentation, such as pay stubs, tax returns, and bank statements, readily available to support your application.

Actionable Steps to Optimize Financing Terms

Implementing these actionable steps can significantly enhance your chances of securing the best possible used car finance rates.

- Check Your Credit Score: Obtain a copy of your credit report and identify any inaccuracies. Take steps to rectify any errors.

- Gather Financial Documents: Compile all necessary financial documents, including pay stubs, tax returns, and bank statements.

- Shop Around: Compare interest rates and terms from multiple lenders, focusing on both online and traditional lenders.

- Negotiate Terms: Don’t hesitate to negotiate the terms of the loan to obtain the best possible interest rate and payment schedule.

- Review the Fine Print: Thoroughly review the loan agreement before signing to ensure that you understand all terms and conditions.

Understanding the Fine Print of Used Car Financing Agreements

Navigating the world of used car financing can feel like navigating a maze. While the initial interest rate and loan term are crucial, the devil is often in the details hidden within the financing agreement. Carefully reviewing these documents is paramount to avoid unpleasant surprises down the road. Understanding the various clauses and potential hidden fees can save you significant money and headaches.

Importance of Thorough Document Review

Thorough review of all loan documents is essential. Failing to scrutinize the fine print can lead to unexpected charges, hidden fees, and unfavorable terms. A comprehensive review ensures you understand the total cost of the loan, including all associated expenses. This proactive approach empowers you to make informed decisions and potentially negotiate better terms.

Common Clauses in Financing Agreements

Used car financing agreements typically include several key clauses. These clauses Artikel the terms and conditions of the loan, protecting both the lender and the borrower. Understanding these clauses is crucial for responsible borrowing.

- Prepayment penalties: Some loans may impose penalties if you pay off the loan early. This clause specifies the amount or percentage of the penalty. These penalties are often calculated as a percentage of the remaining loan balance or a fixed fee. Review the prepayment penalty clause carefully and compare it with other available options. If early repayment is likely, scrutinize this clause to determine the financial impact.

- Late payment fees: This clause Artikels the penalties for late payments, typically expressed as a fixed fee or a percentage of the missed payment. Understanding these fees and the potential accumulation of penalties is vital for responsible financial management.

- Acceleration clauses: These clauses allow the lender to demand immediate payment of the entire loan balance if certain conditions are not met. These conditions often include missed payments, failure to maintain insurance, or violation of other agreement terms. Understanding this clause is critical to avoid defaulting on the loan.

- Default provisions: These clauses Artikel the lender’s recourse if the borrower defaults on the loan. This can include repossession of the vehicle, legal action, and the collection of any outstanding fees.

- Governing law: This clause specifies the jurisdiction’s laws that govern the agreement. Understanding the governing law ensures you are aware of the legal implications and protections afforded to you.

Hidden Fees and Charges

Beyond the stated interest rate, hidden fees and charges can significantly impact the total cost of the loan. These fees often go unnoticed during the initial loan approval process. Common hidden fees include:

- Acquisition fees: These fees cover the administrative costs associated with processing the loan. They are sometimes included in the stated interest rate or as a separate line item. Pay close attention to the exact amount of acquisition fees.

- Document preparation fees: These fees are charged for the preparation and processing of loan documents.

- Late payment penalties: As mentioned earlier, late payment penalties can quickly add up if payments are missed. This clause should be scrutinized to understand the exact amount and how it accrues.

- Prepayment penalties: As discussed earlier, early repayment penalties can significantly impact the total cost of the loan, particularly for those with a plan to repay the loan earlier.

- Insurance fees: Be mindful of any required insurance premiums or associated fees. These fees can be bundled into the monthly payment, making them less noticeable.

Example of a Loan Agreement Clause

“In the event of a default in payment of any installment, the entire unpaid principal balance of the loan, together with accrued interest, late fees, and any other charges, shall become immediately due and payable.”

This clause means that if a single payment is missed, the entire loan balance, including accumulated interest and fees, becomes payable immediately. This can lead to significant financial burden for the borrower. Carefully review this clause and understand the implications of missing payments.

Recent Trends in Used Car Finance Rates

Used car financing rates have experienced dynamic shifts in recent years, influenced by a complex interplay of economic factors and market conditions. Understanding these trends is crucial for both buyers and sellers to make informed decisions in the current landscape. Fluctuations in rates can significantly impact the affordability and accessibility of used car loans.

Recent Changes in Used Car Finance Rates

Used car finance rates have exhibited a noticeable volatility in the past few years, often reacting to broader economic trends. This volatility has made it challenging for both consumers and lenders to predict and manage loan costs effectively. Factors such as inflation, interest rate adjustments, and supply chain disruptions have all played significant roles in these shifts.

Impact of Economic Conditions on Rates

Economic conditions are a primary driver of used car finance rates. High inflation often leads to higher interest rates as central banks aim to curb economic activity. Conversely, periods of economic downturn might see rates fall, but this is often balanced by decreased demand for loans. For instance, during periods of high unemployment, fewer people may qualify for loans, leading to decreased competition and potential increases in rates. A robust job market, on the other hand, tends to increase competition for loans, possibly decreasing rates.

Ongoing Developments in Used Car Financing

Several ongoing developments are reshaping the used car financing landscape. Digital lending platforms are becoming increasingly prevalent, allowing for faster and more convenient loan applications and approvals. Furthermore, the use of alternative data sources to assess creditworthiness is gaining traction. This includes factors like payment history, employment consistency, and even online spending patterns. Such innovation aims to provide more inclusive and efficient access to financing options for consumers with varied credit profiles.

Alternatives to Traditional Financing

Traditional financing methods, while widely available, may not be the best option for all buyers. Alternative financing avenues offer diverse choices, often tailored to specific needs and circumstances. Understanding these alternatives can empower consumers to make informed decisions when seeking used car financing.

Overview of Alternative Financing Options

Alternative financing options for used cars encompass a range of methods beyond traditional loans from banks or credit unions. These options cater to various situations, from those with less-than-perfect credit to those seeking more flexible terms. They include options such as peer-to-peer lending platforms, online financing marketplaces, and specialized dealerships offering unique financing programs.

Advantages of Alternative Financing Options

Alternative financing methods often present advantages over traditional options. These advantages may include faster approval times, more flexible loan terms, and the potential for lower interest rates, depending on the specific circumstances and the lender. Some platforms might offer financing options for those with limited or no credit history.

Disadvantages of Alternative Financing Options

While alternative financing can be beneficial, potential drawbacks exist. These include higher interest rates for borrowers with poor credit or those seeking expedited loan approvals. The complexity of some online platforms or the lack of transparency regarding fees and conditions can also pose a challenge for some buyers. Borrowers must carefully evaluate all fees and terms before agreeing to a financing deal.

Eligibility Criteria for Alternative Financing

Eligibility requirements for alternative financing vary greatly between providers. Factors like credit score, income, debt-to-income ratio, and the desired loan amount significantly influence approval chances. Some lenders may place less emphasis on traditional credit scores, relying on alternative data points such as employment history or payment patterns. This approach can potentially increase access to financing for individuals who might be excluded by traditional lenders.

Comparison of Traditional and Alternative Financing

| Feature | Traditional Financing | Alternative Financing |

|---|---|---|

| Interest Rates | Generally lower for good credit; higher for poor credit | Potentially higher for all borrowers, especially those with lower credit scores |

| Approval Time | Can be several days to weeks | Potentially faster, sometimes within hours or a day |

| Loan Terms | Usually standardized by lender; limited flexibility | Potentially more flexible, offering different payment schedules and loan durations |

| Credit Score Impact | Crucial factor in determining interest rates and approval | Varying importance depending on the lender and the specific program |

| Fees | Generally transparent and clearly Artikeld in the loan agreement | May have hidden or unclear fees, so careful review is essential |

| Customer Service | Often readily available through traditional channels | Customer service may be less accessible or less responsive |